Financial Aid 101: The Types of Aid, Where to Apply, and What You Need to Know About Repayment

by Sequoia Financial Group

by Sequoia Financial Group

Like almost everything else you’re buying, higher education costs have steadily risen over the past 30+ years. In 1980[1], attending a four-year college full-time would cost roughly $10,231 annually (tuition, room and board, and fees included). By the year 2020, that number ballooned by 180%, to $28,775, far out pacing the average inflation rate of roughly 3.3% yearly.

The exponential rise in the cost of higher education means more students require financial assistance to attend a college, university, or career school. In fact, according to the National Center for Education Statistics[2], over 85 percent of students received some form of financial aid in 2020.

If you have a child getting ready for higher education, the search for financial aid might be in your future. Here’s a quick resource you can use to get up to speed on the types of financial assistance that exist, where to apply, and what you need to know about repayment.

Where To Find Aid:

Lots of resources exist to help make college and career schools more affordable (fastweb[3], Edvisors[4], BrokeScholar[5]). Still, we’ll focus on the three most common: the U.S. Department of Education, your state government, and your student’s chosen school.

The U.S Federal Government:

- Federal student aid is available from the U.S. Department of Education and is applied for using the Free Application for Federal Student Aid (FAFSA)[6]. Federal Aid includes:

- Grants – Financial aid that does not have to be repaid (unless a specified act mandates you owe a refund).

- Loans – Borrowed aid that must be repaid with interest.

- Work-Study – Part-time jobs for students with financial needs, allowing them to earn money to help pay education expenses.

- Outside the U.S. Department of Education, you may also qualify for:

- Military aid for serving in the military or being the spouse or child of a veteran tax benefits for education (ex., the American Opportunity or Lifetime Learning Credits; student loan interest deduction)

- An Education Award for community service with AmeriCorps

- Educational and Training Vouchers for current and former foster care youth

- Scholarships and loan repayment through the Department of Health and Human Services’ Indian Health Service, National Institutes of Health, and National Health Service Corps

State Government

Even if you are not eligible for federal aid or seek assistance in addition to what is awarded through federal programs, you might qualify for financial aid from your state. Every state has its funds and process for distributing aid, often including grants and scholarships. Contact your state grant agency for more information[7].

Specific state aid packages are distributed on a “first come, first serve” basis. Complete your FAFSA form early to maximize your eligibility for financial aid.

Your College or Career School

Surprisingly, many educational institutions offer financial aid.

Colleges and career schools typically offer two types of financial aid: need-based and merit-based. Need-based aid addresses the student’s financial needs based on the FAFSA eligibility formulas, while merit-based financial aid rewards students for some form of academic or extracurricular success. To learn what may be available:

- Visit the financial assistance page on the selected school’s website.

- Ask the department that offers your course of study; there may be a scholarship opportunity for students in your major.

- Fill out any applications the school requires for aid and meet the deadlines. Many schools require students to submit the College Scholarship Service Profile (CSS/Financial Aid PROFILE) and the FAFSA.

Eligibility for Financial Aid

The Student Aid Index (SAI) is an eligibility index for student aid, not a determination of what an applicant will pay. It identifies applicants with the greatest need. The equation is calculated based on the student’s and parents’ (if applicable) income, asset, tax, and demographic information on the FAFSA.

The income and assets of extended family members, like grandparents, are not considered in federal financial aid formulas. That means 529 accounts owned by grandparents or extended family members will no longer negatively impact financial aid eligibility, nor will cash support received from such individuals. The new form, the amount of a student’s total income, which includes untaxed income, will come directly from the federal income tax return via the IRS Data Retrieval Tool.

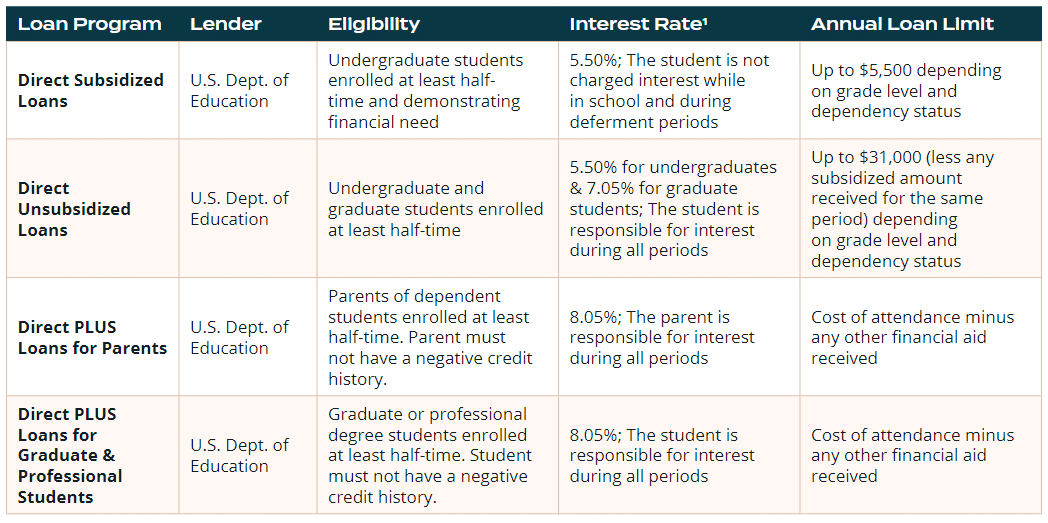

Compare the Federal Student Loan Programs

In addition to federal loan programs, private loans may help fill the gap for student aid. However, these loans tend to have higher interest rates and less flexible repayment options than those offered by the U.S. Department of Education.

Don’t Get Left “A Loan”

Planning and paying for higher education can feel like walking on a high wire without a net. Don’t get overwhelmed. Speak with a Sequoia Financial Advisor so that when you send your family member to college, you can do so with clarity and confidence.

Sources:

- https://www.forbes.com/advisor/student-loans/college-tuition-inflation/

- https://nces.ed.gov/programs/digest/d21/tables/dt21_331.20.asp

- https://www.fastweb.com/

- https://www.edvisors.com/

- https://brokescholar.com/

- https://studentaid.gov/h/apply-for-aid/fafsa

- https://www.nasfaa.org/State_Financial_Aid_Programs

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Major Equity Indices Decline as Post-Election Euphoria Fades