Stocks Rally After Softer-Than-Expected Core Inflation

by Sequoia Financial Group

by Sequoia Financial Group

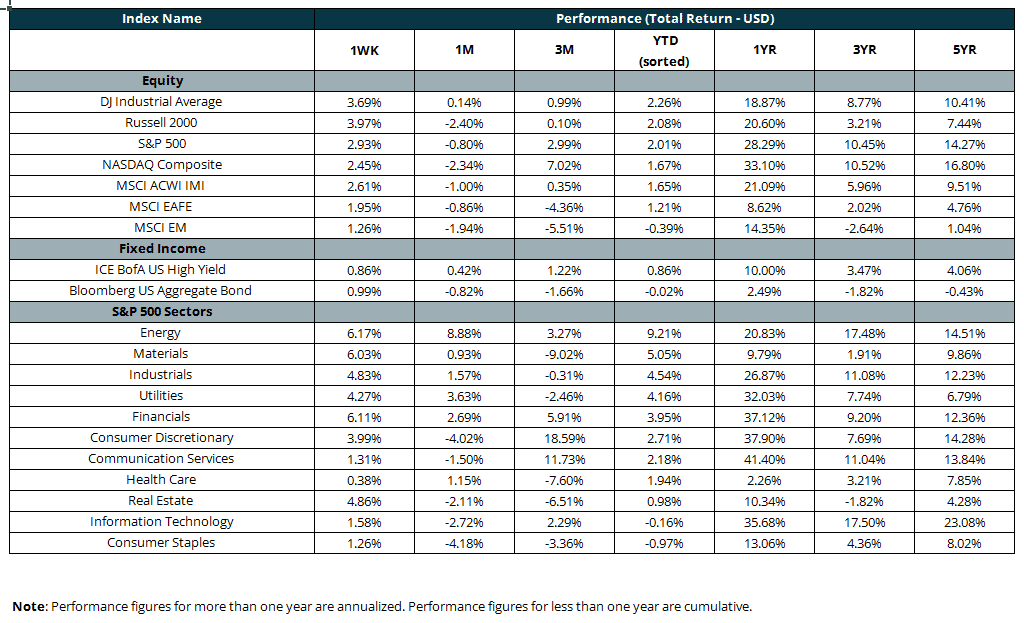

The S&P 500 rose 2.9% last week in response to a soft core Consumer Price Index inflation (CPI) reading.1 Core (excluding food and energy) CPI rose 0.2% month over month (m/m), lower than the 0.3% expected increase. Core CPI rose 3.2% year over year (y/y), down from the 3.3% y/y increase last month.2

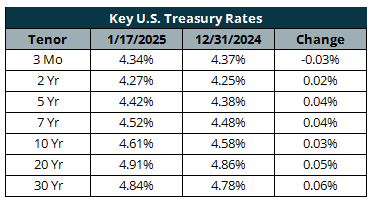

Interest rates declined following the news, as bond markets anticipated a higher probability of cuts to the Fed funds rate.3 The 10-year Treasury yield, which influences discount rates used to value stocks, declined to 4.61% from 4.77%.4 Absent changes in earnings expectations, lower discount rates drive equity valuations upward.

Despite the decline in Core CPI, headline CPI increased m/m, in line with expectations. The 2.6% m/m increase in energy prices, particularly gasoline (+4.4% m/m), was a notable driver.2 The Federal Reserve prefers core measures of inflation, specifically the core Personal Consumption Expenditures (CPE) price index, to guide its interest rate policy. The next release of the PCE will be on Friday, January 31.5

Bond prices rose given the decline in interest rates, leading to a 1% rise in the Bloomberg US Aggregate Bond Index (an index of investment-grade bonds). The Bloomberg US Corporate High-Yield Index rose 0.8%.1

Banks kicked off a strong start to the Q4 earnings season. JPMorgan Chase (JPM), the biggest US bank by total assets, beat earnings expectations by 17.5%. CEO Jamie Dimon highlighted the resilience of the US economy and healthy consumer spending.6 JPM is up 8.7% year to date (YTD), and the S&P 500 Banks Index is up 7.9%.1

Magnificent 7 (“Mag 7”) names continue to outperform the broader stock market this year, except for Apple (AAPL). One research firm noted that Apple’s iPhone unit shipments to China declined by 17% for the full year 2024. Chinese companies Huawei and Vivo have taken the top two spots of China’s market share, leaving Apple in third place.7 AAPL is down 8.2% YTD.1

Over the remaining earnings season, many investors are searching for more “breadth” in the stock market. Recent gains have been concentrated in the Mag 7. The equal-weighted S&P 500 Index, an indicator of broad stock market performance, returned 12.8% last year relative to the market-weighted S&P 500’s return of 25.0%.1 Catalysts other than AI spending may need to materialize for the other 493 stocks to outperform. Strong bank earnings are a good start.

Sources

1Morningstar Direct

2https://www.bls.gov/news.release/cpi.nr0.htm

3https://www.wsj.com/economy/central-banking/cpi-report-inflation-december-interest-rate-0347479e

4https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value_month=202501

5https://www.bea.gov/data/personal-consumption-expenditures-price-index

6FactSet

7https://finance.yahoo.com/news/why-apple-aapl-shares-falling-185322097.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets