Financial Markets Continue to Climb a Wall of Worry

by Sequoia Financial Group

by Sequoia Financial Group

With fourth quarter earnings releases largely in the rear-view mirror, market watchers turned their attention back to economic reports last week. But before the release of major inflation updates mid-week, President Trump took center stage on Monday and announced 25% tariffs on all imported aluminum and steel. Prices of both products spiked higher on the news. However, Trump did not say when the tariffs would be imposed. He further announced retaliatory tariffs on countries that charge tariffs on US goods, but the timetable for those tariffs was also unclear. With no firm implementation dates, the broad stock market indices largely looked past the announcements and moved higher to start the week.[1]

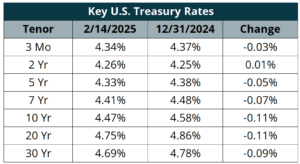

The release of the latest report on consumer prices on Wednesday stalled the market’s advance, however. The January consumer price index (CPI) jumped 0.5% while annual inflation climbed 3%.[2] Both readings came in a little hotter than expected and signaled interest rates could stay higher for longer. Indeed, the 10-year Treasury yield jumped to 4.66% on the news and the bond market erased most of its early year gains. After initially dropping more than 400 points, the Dow Jones Industrial Average recovered some ground and ended the day losing 225 points (0.50%). Stock market losses could have been steeper, but House Speaker Johnson said the White House was considering tariff exemptions for pharmaceuticals and autos, helping Lilly, General Motors, and Ford end the day higher.[3]

Inflation concerns eased a bit on Thursday with the release of the producer price index (PPI), which measures wholesale price inflation. The headline reading jumped 0.4%, and like CPI came in a little higher than expected. However, excluding the volatile food and energy components, the index climbed just 0.3% and that number was in line with forecasts.[4] Stocks and bonds staged a relief rally on the news, with the Dow more than recovering its CPI-driven losses. The NASDAQ fared even better, jumping 1.5%. The tech-heavy index got an added lift from Nvidia, which rallied after Hewlett Packard announced its first product shipments incorporating Nvidia’s advanced-AI Blackwell chip. Meanwhile, bond priced pushed higher and yields lower, with the 10-year Treasury yield dipping back to 4.53%.[5]

Stocks were mixed on Friday, but ended the week with solid gains. The NASDAQ gained 2.3% for the week, while the Dow Jones Industrials moved 0.9% higher. Looking ahead, we’ll have a quieter week on the economic front, with employment and consumer sentiment in focus. But we expect the ongoing news flow from Washington DC will continue to affect the markets.

[1] https://www.cnbc.com/2025/02/09/stock-futures-edge-lower-ahead-of-economic-data-threat-of-fresh-tariffs.html

[3] https://www.cnbc.com/2025/02/11/stock-market-today-live-updates.html

[4] https://www.bls.gov/news.release/pdf/ppi.pdf

[5] https://www.cnbc.com/2025/02/12/stock-market-today-live-updates.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Markets Soar After 90-Day Tariff Pause