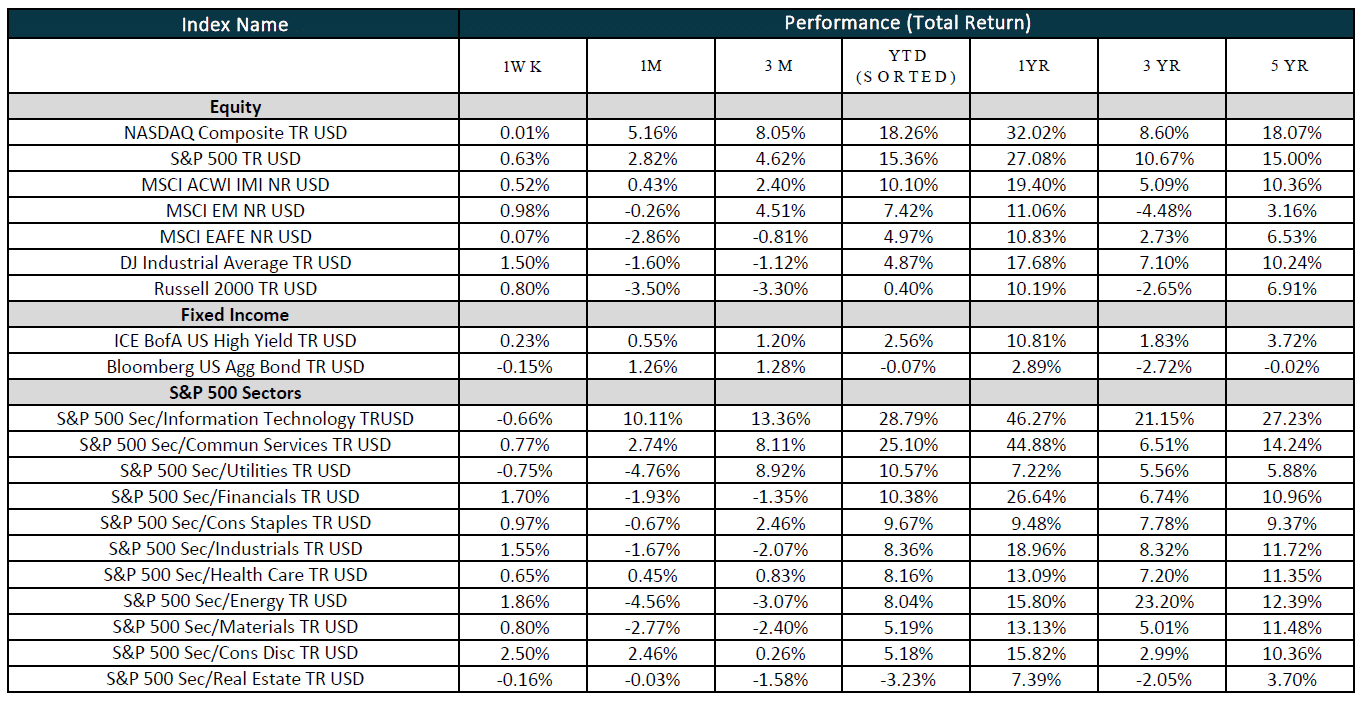

US equity markets started out strong in a mostly quiet week of trading but lost some steam towards the end of the week on softer economic data. They finished mostly higher for week with the equal-weighted S&P outperforming the official index. The NASDAQ Composite was the week’s underperformer although Big Tech was mostly higher; Nvidia was the notable laggard.

US equities finished on an up note in Monday trading, ending near highs after shaking off some early morning weakness. Not many catalysts were behind the risk-on move. Although the path of least resistance appears higher given more certainty around the Fed rate cut path, disinflation traction, AI secular growth tailwinds, and favorable earnings revision, these trends were offset by weak breadth and global political uncertainty.

On Tuesday, US equities finished near highs. Though Big Tech was the relative underperformer, Nvidia was a notable gainer and overtook Microsoft as the world’s largest company. Headline May retail sales rose +0.1% m/m, lower than estimates of +0.3%, while April’s headline was revised down to 0.4%.1 Retail sales ex-auto fell 0.1% m/m vs. estimates of +0.2%. Headline results were driven partially by lower gas prices with retail sales excluding gasoline rising 0.3%.1 Five of the thirteen tracked categories saw declines reflecting cooling consumer spending.

Markets were closed on Wednesday in observation of the Juneteenth holiday.

US equities ended the day lower on Thursday with the NASDAQ leading on the downside as recent AI winners consolidated. Nvidia and Apple were notable laggards on the day. Macro data came in softer than expected. Initial jobless claims at 238K tracked estimates of 235K, which had seen an increase in recent weeks.2 May housing starts at 1.277M missed estimates of 1.39M, falling 5.5% m/m vs. estimates of a 1.1% increase.3 Single-family housing starts were 949K, declining 2.9% from April’s 977K starts.3

US equities were mixed in Friday’s session. Big Tech was mostly higher, with Nvidia a notable decliner. AI, semiconductors, and momentum stocks were lower for the second straight session with Nvidia breaking an 8-week winning streak during which it rallied ~75%. In contrast to Thursday’s softer batch of economic data, June flash PMIs beat on the upside, coming in at 54.6 vs estimates of 53.4.4 Services came in at 55.1 vs estimates of 53.5, its highest reading since April 2022. 4 The report noted selling price inflation fell to its lowest levels in four years, helping to slow the growth in input costs. 4 Elsewhere, May existing home sales came in at 4.11M, in line with estimates and showed inventories at their highest levels in four years.5

Sources

- https://www.census.gov/retail/marts/www/marts_current.pdf

- https://www.dol.gov/ui/data.pdf

- https://www.census.gov/construction/nrc/pdf/newresconst.pdf

- https://www.pmi.spglobal.com/Public/Home/PressRelease/dab295292d5a444c8f772b2b82587fa2

- https://www.nar.realtor/newsroom/existing-home-sales-edged-lower-by-0-7-in-may-as-median-sales-price-reached-record-high-of-419300

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Stocks Extend Rally on Trade and Earnings Positives