Cooling Inflation Provides Needed Relief for Stocks

by Sequoia Financial Group

by Sequoia Financial Group

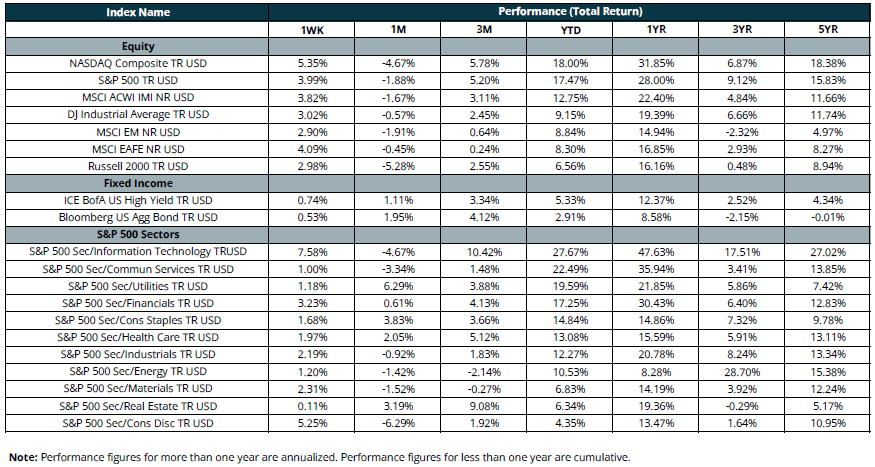

The financial markets turned their attention to inflation last week. Consumer inflation has been moving steadily lower since peaking at 9% in June 2022. Two years later it stood at just 3%.[1] But continued progress in July toward the Federal Reserve’s stated 2% inflation target could give the Fed the green light it’s looking for to finally cut interest rates.

The first hint of a positive reading came on Tuesday with the monthly Producer Price Index (PPI) – a measure of wholesale prices. PPI increased only 0.1% in July, while economists had expected a 0.2% bump. For the trailing 12 months, PPI advanced just 2.2%. The S&P 500 and the Dow jumped more than 1% on the news, and the NASDAQ rallied more than 2%. Meanwhile, Starbucks soared 21% after announcing it had tapped Chipotle CEO Brian Niccol to be its new CEO.[2] Niccol’s work at Chipotle helped the stock to an 800% gain during his tenure[3], so hopes are high.

The rally continued on Wednesday as the Consumer Price Index (CPI) demonstrated more signs of slowing inflation by climbing just 0.2% in July, in line with expectations. For the trailing 12 months, consumer prices moved 2.9% higher, grinding slowly toward the Fed’s target.[4] The two benign inflation reports provided added support for the Fed to cut rates at its next meeting in September. At week’s end, the odds of a rate cut stood at 100%.[5] The only remaining question for the Fed was whether to cut rates a quarter per cent (75% chance) or half a per cent (25% chance). In other developments, Kellanova (formerly the Kellogg snacking brands) stock jumped 8% on news that it would be acquired by privately-held Mars.[6]

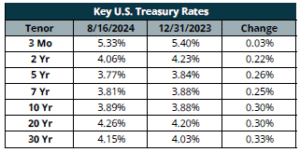

Positive economic reports on Thursday pushed markets higher still. The health of the consumer had become a concern in recent weeks, as weak job numbers spurred recession worries. But retail sales jumped 1% in July, and jobless claims dropped, mitigating those concerns.[7] For the week, the benchmark S&P 500 Index jumped nearly 4%, while the NASDAQ rallied more than 5%.[8] On the fixed-income front, bond prices moved slightly higher.

We’ll be monitoring the remaining few earnings reports this week, with Palo Alto Networks, Target, and Lowe’s due to report. And we’ll get a good look at the housing market, with reports on new and existing home sales coming later in the week. Finally, the Federal Reserve Bank of Kansas City will host global central bankers at its annual Economic Policy Symposium in Jackson Hole, Wyoming. Fed Chairman Powell will be the keynote speaker – he’s unlikely to confirm a rate cut, but he will provide an updated outlook on the economy and interest rates.

[1] https://www.bls.gov/opub/ted/2024/consumer-prices-up-3-0-percent-from-june-2023-to-june-2024.htm

[2] https://www.cnbc.com/2024/08/12/stock-market-today-live-updates.html

[3] https://stories.starbucks.com/press/2024/starbucks-names-brian-niccol-as-chairman-and-chief-executive-officer/

[5] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html?redirect=/trading/interest-rates/countdown-to-fomc.html

[6] https://www.cnbc.com/2024/08/13/stock-market-today-live-updates.html

[7] https://www.cnbc.com/2024/08/14/stock-market-today-live-updates.html

[8] https://www.cnbc.com/2024/08/15/stock-futures-are-little-changed-as-wall-street-heads-for-a-winning-week.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets