Inflation Numbers Fail to Move Markets

by Sequoia Financial Group

by Sequoia Financial Group

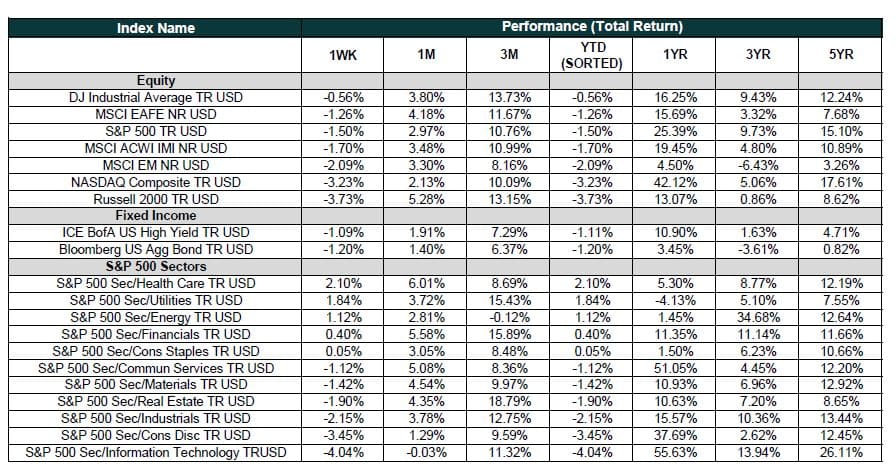

Equity markets started last week strong, with the S&P 500 and NASDAQ Composite gaining 1.4% and 2.2% respectively on Monday. The rebound followed the stock market’s first losing week since October.[1] Bargain hunters bid tech stocks higher, with Amazon, Apple, Alphabet, and Nvidia all gaining. Nvidia was the big winner, rallying more than 6% to reach an all-time high. It then eclipsed that high on Tuesday, Wednesday and Thursday.[2] The stock reached $553/share before pulling back a bit. For comparison, one year ago Nvidia closed at just $170/share. Boeing, on the other hand, slumped 8% on Monday, after a door plug on one of its Alaska Airlines planes blew out mid-flight.[3] The incident pushed the FAA to ground Boeing 737 Max 9 models with a plug door until the planes could be inspected.

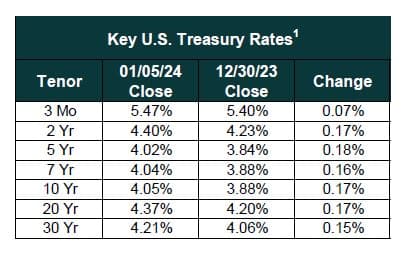

Later in the week, the market turned its attention to inflation and the Federal Reserve’s possible reaction to it. The Consumer Price Index (CPI) came in slightly hotter than expected on Thursday.[4] Expectations were for a modest monthly increase of 0.2%, but CPI increased 0.3% in December. The annual rate now stands at 3.4%, still ahead of the Federal Reserve’s 2% target. Surprisingly, stocks were little changed on the news. Further, the odds of an interest rate cut in March held firm at 65%[5], despite the higher-than-expected CPI number and Cleveland Fed President Loretta Mester saying in a Bloomberg interview that more work needs to be done on inflation and that a rate cut in March could be premature.[6]

The Producer Price Index (PPI) delivered a friendlier report for the stock market on Friday, but again share prices were little changed.[7] PPI, which measures wholesale prices, was expected to gain 0.1% in December but it actually fell by that amount. For the trailing 12 months, PPI crept higher by just 1%.

Friday also brought a slew of bank earnings reports. Results were affected by one-time charges associated with the FDIC clean-up of Silicon Valley Bank and Signature Bank. Large banks will be responsible for replenishing the $16 billion used by the FDIC to cover uninsured depositors.[8] JP Morgan, Wells Fargo, and Bank of America, which all reported earnings on Friday, ended the day lower.

Stock market averages ended the week higher, but two weeks into the new year remain little changed from year-end 2023. With the Fed likely on hold until March, we expect Q4 earnings will drive markets over the next few weeks. On tap this week, more financials, with Q4 reports due from Morgan Stanley, Goldman Sachs, Charles Schwab, Discover Financial, and others.

[1] https://finance.yahoo.com/news/p-500-just-did-something-104500713.html

[2] https://www.investors.com/market-trend/stock-market-today/dow-jones-futures-cpi-inflation-report-nvidia-stock-set-to-hit-record-high/

[3] https://www.cnbc.com/2024/01/07/stock-market-today-live-updates.html

[4] https://www.cnbc.com/2024/01/10/stock-market-today-live-updates.html

[5] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html?redirect=/trading/interest-rates/countdown-to-fomc.html

[6] https://www.reuters.com/markets/us/feds-mester-says-march-probably-too-early-rate-cut-2024-01-11/

[7] https://www.cnbc.com/2024/01/11/stock-market-today-live-updates.html

[8] https://www.ft.com/content/c55c06f9-5de1-49e5-a9c5-770a885dab67

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Growth Concerns Put Pressure on Richly Priced US Stocks