Major Inflation Readings Bring Smoke, but No Fire…So Far

by Sequoia Financial Group

by Sequoia Financial Group

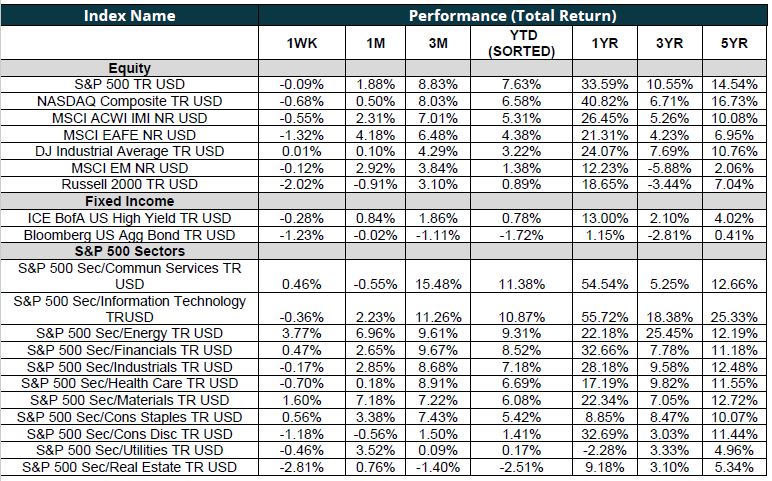

Markets entered last week looking for evidence that inflation was continuing its slide toward the Federal Reserve’s stated 2% target. The Consumer Price Index (CPI) released on Tuesday was expected to show an annual increase of 3.1%, but it came in slightly higher at 3.2%[1]. Though the overall CPI data missed expectations, underlying price changes supported the argument that inflation remains under control. Indeed, food prices were flat, and medical services costs and new vehicle prices actually dropped[2].

And the stock market responded favorably to the print, with the S&P 500 rallying to close Tuesday at a new all-time high. Technology stocks led the charge, with Nvidia jumping more than 7% and Meta climbing more than 3%. Oracle also contributed to the market’s rally, following a strong earnings report after the market closed on Monday. Cloud growth helped Oracle’s total revenue increase 7% year over year, and remaining performance obligations were up 29%[3]. Like the S&P 500, Oracle reached a new high on Tuesday.

Unfortunately, Tuesday proved to be the lone bright spot for the week. Wednesday was marred by profit taking in technology stocks and negative headlines for Tesla, US Steel, and Dollar Tree[4]. Tesla was downgraded by Wells Fargo and traded close to its lowest level in a year. US Steel, which has an offer to be purchased by Nippon Steel, traded lower after President Biden expressed concern about the deal. And Dollar Tree posted disappointed earnings, which weighed not only on its own stock but also that of rivals Five Below and Dollar General. And Thursday, wholesale inflation, as measured by the Producer Price Index, came in a bit hotter than anticipated. Energy prices posted their biggest increase since August and headline PPI climbed 1.6% for the 12 months ending in February[5].

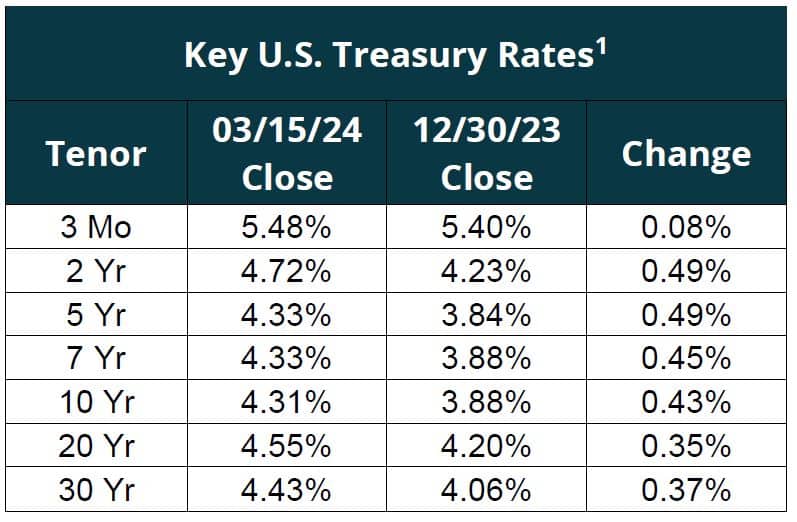

Meanwhile, the bond market had no bright spots last week. Bond yields moved higher throughout the week, pushing prices lower. The 10-year Treasury yield ended the week near its high mark for the year, at just over 4.3%[6]. And the benchmark Bloomberg Aggregate Bond Index now sits at a 1.72% loss for the year through March 15.

Attention now turns to the Federal Reserve, which meets on Tuesday and Wednesday of this week. The somewhat heated inflation numbers have pushed expectations of the first Fed rate cut out to June or July[7], so no big announcement is expected. However, the market will be tracking the Fed’s quarterly dot plot, which shows the Fed’s own prediction of future interest rates, as the S&P 500 looks to end a two-week losing streak.

[1] https://www.cnbc.com/2024/03/11/stock-market-today-live-updates.html

[2] https://www.bls.gov/news.release/pdf/cpi.pdf

[3] https://investor.oracle.com/investor-news/news-details/2024/Oracle-Announces-Fiscal-2024-Third-Quarter-Financial-Results/default.aspx

[4] https://www.cnbc.com/2024/03/12/stock-market-today-live-updates.html

[5] https://www.cnbc.com/2024/03/13/stock-market-today-live-updates.html

[6] https://finance.yahoo.com/quote/%5ETNX

[7] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html?redirect=/trading/interest-rates/countdown-to-fomc.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets