Market Rebound Attempt Fails

by Sequoia Financial Group

by Sequoia Financial Group

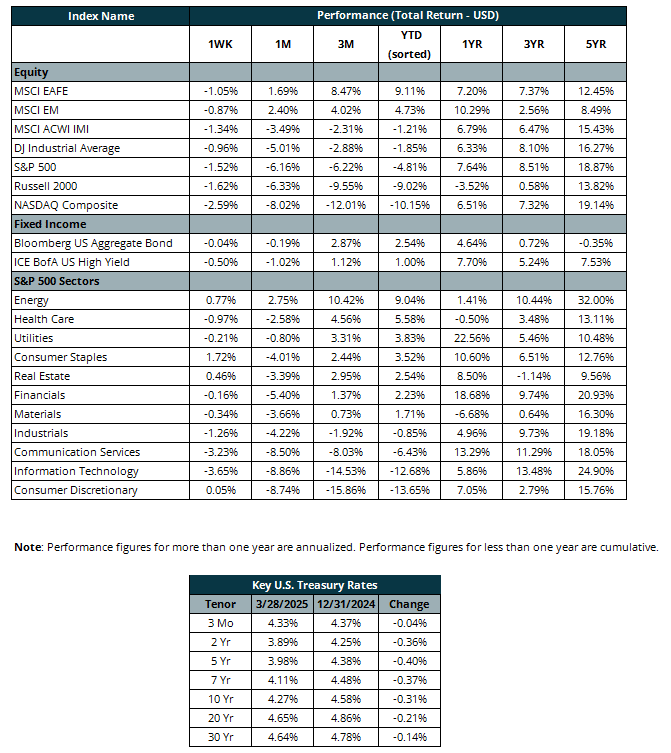

Looking to build on the first winning week in five, stocks started last week strong. President Trump had been broadcasting a plan for reciprocal tariffs that would be announced on April 2, going so far as to label it “Liberation Day”. A lack of details on the plan had the stock market on edge in recent weeks, but an announcement on Monday implied the tariffs would be narrower in scope and not as punishing to certain sectors. A relief rally pushed the NASDAQ higher by 2.3% and the S&P 500 up 1.8%.[1]

The joy was short-lived, however, as President Trump announced 25% tariffs on imported cars and trucks on Wednesday afternoon. Further, he described the auto tariffs as “permanent”, likely removing any chance of a quick removal or delay. The United Auto Workers Union applauded the move, which could ultimately lead to greater U.S. auto production. But Wedbush Securities analyst Dan Ives wrote in a research note that the tariffs would push the average price of cars up $5,000-$10,000. Ives described the 25% tariff as “almost an untenable, head-scratching number for the U.S. consumer” .[2] Stocks slumped on the tariff news, with automakers the biggest losers. The NASDAQ gave back 2% and the S&P 500 slipped 1.1%.[3] But General Motors fell more than 10% from Wednesday morning through Friday afternoon[4], while Ford dropped more than 5%[5].

The sell-off continued on Friday, when hotter-than-expected inflation and weak consumer sentiment pushed buyers to the sidelines. The Federal Reserve’s favored inflation measure – the personal consumption expenditure index (PCE) – rose 2.8% in February, a bit higher than the 2.7% analysts had expected, and above January’s 2.6% number. The Fed continues to target 2% inflation, but that target was last reached in February 2021. And Fed Chairman Powell doesn’t expect to reach that level in 2025.[6] Meanwhile, consumer sentiment reached its lowest level since November 2022, with consumers worried about unemployment climbing and inflation worsening.[7] Overall, the S&P 500 dropped 1.5% for the week, while the NASDAQ slid 2.6%. The bond market had a bumpy week, but ended the week little changed overall.

The tariff roller coast continues this week, with President Trump’s April 2 reciprocal tariff announcements. On the plus side, the European Union is looking at concessions that could be made as part of a negotiated agreement.[8] Here’s hoping an agreement comes sooner rather than later and markets can get back on track.

[1] https://www.cnbc.com/2025/03/23/stock-market-today-live-updates-.html

[2] https://www.freep.com/story/news/politics/2025/03/26/trump-all-imported-autos-face-25-tariff-beginning-april-2/82674427007/

[3] https://www.cnbc.com/2025/03/25/stock-market-today-live-updates.html

[4] https://finance.yahoo.com/quote/GM/

[5] https://finance.yahoo.com/quote/F/

[6] https://www.cnbc.com/2025/03/19/fed-meeting-live-updates.html

[7] https://www.cnbc.com/2025/03/27/stock-market-today-live-updates.html

[8] https://www.investing.com/news/stock-market-news/eu-identifies-concessions-to-alleviate-impending-us-tariffs–bloomberg-93CH-3954584

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets