Market Rebound Driven by Tech Earnings and Easing Trade Tensions

by Sequoia Financial Group

by Sequoia Financial Group

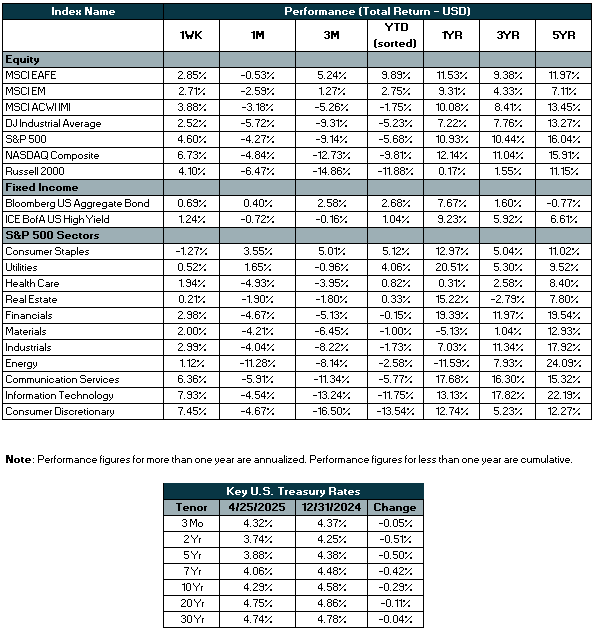

U.S. stocks rebounded sharply this week after a volatile start, driven by easing concerns over trade policy and reassurance from President Trump regarding tariffs. Strong tech earnings and softening trade rhetoric fueled the rally, with the Nasdaq surging 6.7%. Meanwhile, U.S. bond yields dropped, easing market volatility, while the IMF downgraded global growth forecasts amid rising tariff risks. Economic data showed resilient consumer spending but continued weakness in housing, leaving markets uncertain about future Fed actions.

U.S. stocks staged a strong comeback this week after a rocky start. The major indexes fell sharply on Monday — with the Dow down nearly 972 points (2.5%), the S&P 500 off 2.36%, and the Nasdaq losing 2.55% — amid renewed concerns over U.S. trade policy and political tensions involving the Federal Reserve. Midweek, President Trump’s softer stance on tariffs against China and reassurances regarding the Federal Reserve’s independence calmed earlier fears and triggered a relief rally. Markets rebounded over the next four days, fueled by easing tariff worries and reassurance over Fed leadership. The Nasdaq surged 6.7% for the week, the S&P 500 rose 4.6%, and the Dow gained 2.5%, erasing the previous week’s losses.

The rally was primarily driven by strong earnings from major technology companies and a softening in trade rhetoric. Tech stocks in the S&P 500 climbed nearly 8% for the week, propelling the Nasdaq back into positive territory for April. Strong quarterly results from major tech companies — including Alphabet, Tesla, Nvidia, and Meta — boosted sentiment, with over 70% of S&P 500 companies beating earnings expectations. Defensive sectors, like consumer staples, lagged. Earnings momentum continued to build, with S&P 500 first-quarter net income now projected to grow 10.1% year-over-year, up from 7.0% a week earlier. Thursday’s rally was especially strong, fueled by gains in mega cap tech names, though sector leadership remains broader than in past tech-driven rebounds.

U.S. government bond prices rose this week, sending yields lower and easing the extreme volatility gripping the fixed-income market. The 10-year Treasury yield closed around 4.26% on Friday, down from a recent intraday high of 4.59% on April 11, while the 30-year yield settled near 4.72%. Earlier in April, the bond market had experienced one of its sharpest moves in years, driven by fears that rising tariffs would stoke inflation and by concerns over the safe-haven status of Treasuries amid rumored selling by China and Japan. Liquidity deteriorated as investors shifted into short-term T-bills, but by late April, yields on both the 2-year and 10-year notes had moderated. Meanwhile, the U.S. dollar weakened for a sixth consecutive week, reflecting reduced confidence in the U.S. as a global haven.

The International Monetary Fund lowered its global and U.S. growth forecasts, citing rising tariff risks and escalating trade tensions. It now projects global GDP growth of 2.8% in 2025 and 3.0% in 2026, down from 3.3% previously. It also cut its 2025 U.S. growth forecast to 1.8%, a 0.9 percentage point downgrade from January. While not forecasting a U.S. recession, the IMF raised its recession odds to 40%, up from 25% in October 2024.

U.S. consumer sentiment, measured by the University of Michigan, extended its steep year-to-date decline in April, falling for the fourth consecutive month to 52.2 — down from 57.0 in March and 74.0 at the end of 2024 — amid growing concerns about tariffs, inflation, and economic risks. Despite an upward revision from the preliminary 50.8 reading, the expectations index plunged to 47.3, the lowest since July 2022, while year-ahead inflation expectations surged to 6.5%, the highest since 1981, driven by trade policy uncertainty.

Meanwhile, consumer spending remained resilient in March, with retail sales beating expectations as consumers likely accelerated purchases to avoid future tariff-driven price hikes. However, housing data pointed to underlying strain: housing starts fell sharply due to high prices and mortgage rates, and existing home sales slumped by 5.9% to a 4.02 million annualized rate — the steepest drop in over two years — though a rise in building permits hinted at strength in multifamily construction.

In the coming week, investors will focus on a wave of corporate earnings alongside key economic data releases, including the initial estimate of first-quarter GDP, an update on inflation, and the April jobs report, which will show how employment growth compares with March’s stronger-than-expected gain of 228,000 jobs.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Market Rebound Driven by Tech Earnings and Easing Trade Tensions