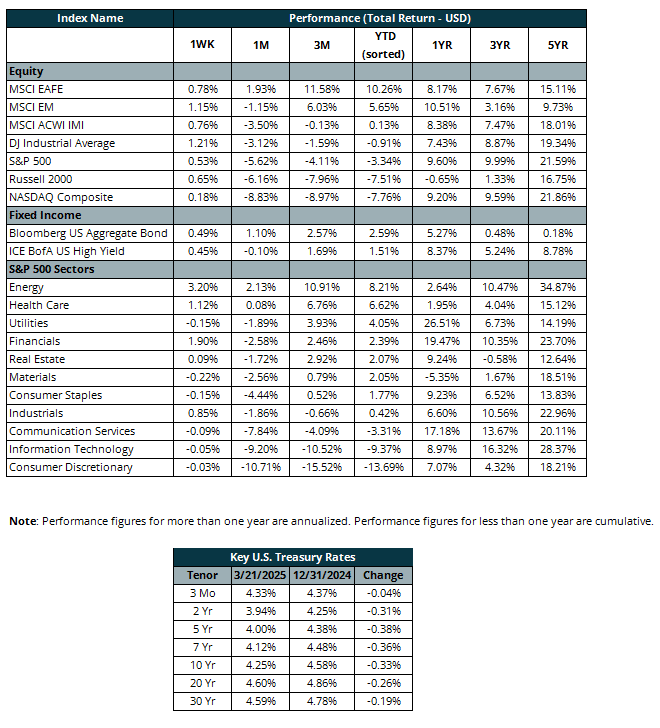

The S&P 500 opened Friday’s session on pace to extend its weekly losing streak to five. But the Index rallied in the afternoon to end the week up 0.5% and year-to-date down 3.3%.[1]

In response to an uncertain economic backdrop, companies have been sounding a cautious tone. Nike (NKE) and FedEx (FDX) joined the list of firms that have recently cut earnings guidance. Nike expects its current quarter sales will decline more than feared due to several external factors, including tariffs, geopolitical dynamics, and consumer confidence.[2] NKE was down 5.5% on Friday, despite beating earnings expectations by 80%.1[3] FDX was also down on Friday (-6.5%) after management noted that continued weakness in the industrial economy has weighed on customer demand.1[4]

The Federal Reserve echoed the concerns of the private sector. The Federal Open Market Committee (FOMC) downgraded its 2025 real GDP growth forecast to 1.7% from 2.1%. The FOMC also increased its unemployment projection by 0.1% to 4.4% and core PCE inflation by 0.3% to 2.8%. [5] Fed Chairman Jerome Powell noted a moderation in consumer spending and a potential increase in prices owing to tariffs, but also said that tariff inflation could be transitory. Therefore, the FOMC continues to forecast two rate cuts for the year.[6] It is worth noting that Powell incorrectly believed inflation in 2021 was transitory, and the FOMC was slow to hike rates. Headline inflation was 9% by June 2022, the highest reading in several decades.[7]

Recent equity market volatility underscores the benefits of holding a portfolio diversified across asset classes. Bond prices and interest rates have an inverse relationship: prices rise as rates decline. Bond markets have priced in a higher probability that the Fed will have to cut rates in response to a recession. The Bloomberg US Aggregate Bond Index is up 2.6% on the year.1 High-yield bonds have also offered diversification: for example, the Bloomberg US Corporate High-Yield Index is up 1.5%.1

Given the recent sell-off, many market participants are considering “buying the dip.” The S&P 500 currently trades at a price-to-earnings (P/E) ration of 20.4x, which is significantly cheaper than the 22.5x level seen in December 2024. However, considering that the forward P/E over the past 10 years has averaged 18.6x, the S&P 500 still might not be cheap.3 Sequoia Research will be closely monitoring developments on tariffs which, if fully enacted, could have a material impact on earnings growth.

[1] Morningstar Direct

[2] https://www.cnbc.com/2025/03/20/nike-nke-q3-2025-earnings.html

[3] FactSet

[4] https://www.wsj.com/business/earnings/fedex-cuts-outlook-despite-higher-profit-sales-806f91b5

[5] https://www.cnbc.com/2025/03/19/fed-rate-decision-march-2025.html

[6] https://www.wsj.com/economy/central-banking/fed-forecast-inflation-tariffs-trump-economy-5a5098a1?mod=economy_feat2_central-banking_pos5

[7] U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items in U.S. City Average [CPIAUCSL], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CPIAUCSL, March 23, 2025

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Stocks Extend Rally on Trade and Earnings Positives