No ‘Santa Claus Rally’ in 2024, But Stocks Didn’t Need One

by Sequoia Financial Group

by Sequoia Financial Group

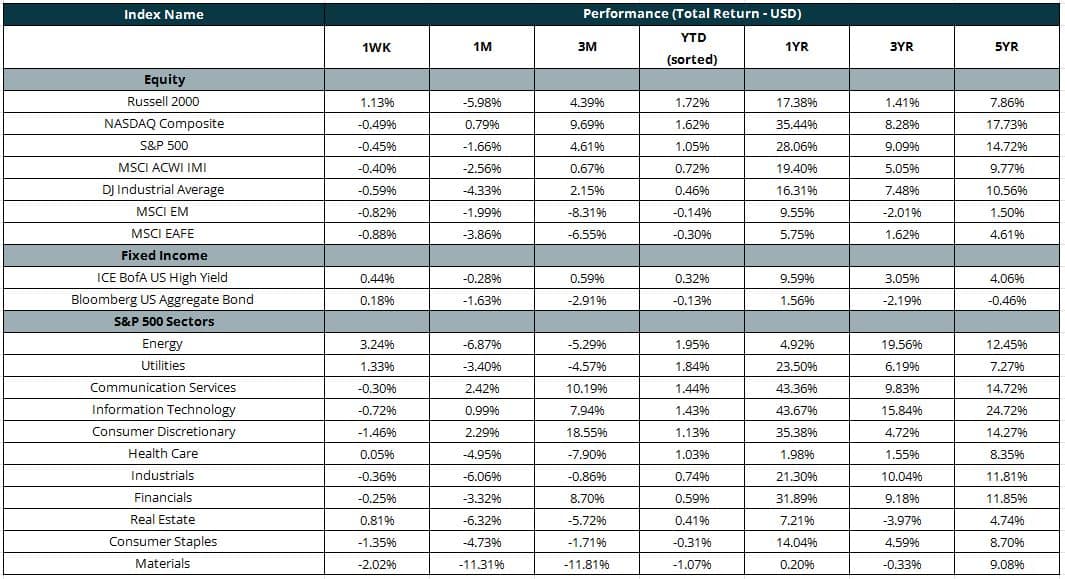

Stocks typically end calendar years and start new ones on a high note. The final five trading days of December and the first two trading days of January have seen the S&P 500 gain an average of 1.3% since 1950 and register positive results nearly 80% of the time – the so-called Santa Claus Rally.[1] The Rally didn’t happen in 2024/2025 but stock investors aren’t likely complaining much: the S&P 500 closed the year with a 23% return, while the tech-heavy NASDAQ powered 29% higher.[2]

Fixed-income investors had less to cheer. After starting the year strong on the hope than Fed rate cuts would provide a lift to bond prices, the Morningstar Core Bond Index limped to a 1.4% return for the year. The index was on track for a mid-single-digit showing, but lost 3% in the fourth quarter as the Federal Reserve dialed back rate cut expectations.[3] Sticky prices remained a concern for Fed Chairman Powell, as consumer inflation failed to reach the Fed’s 2% target.

Stocks and bonds enter 2025 with arguments in their favor, but also concerns. Factset projects S&P 500 earnings to grow 14.8% in 2025 after growing an estimated 9.5% in 2024.[4] Higher earnings could support higher stock prices, and indeed Goldman Sachs, Morgan Stanley, Bank of America and others project the S&P 500 will return more than 10% in 2025.[5] Trump 2.0 could also provide a lift to stock prices, as the new administration looks to cut red tape and implement measures to support the US economy. Bonds may not be able to rely on multiple Fed rate cuts for price gains, but bond yields could provide a nice return if prices simply hold where they are. The 10-year Treasury yield topped 4.5% Friday, and the yield on the Bloomberg US Corporate Bond Index checks in at 5.4%.[6]

But lofty stock valuations and stubborn inflation could get in the way of another exceptionally strong year for stocks, and hamper a bond market recovery. The forward price/earnings ratio for the S&P 500 now stands at 21.4 versus the five-year average of 19.7.4 Meanwhile, higher-than-expected inflation could push bond yields higher and bond prices lower.

Though the conflicting narratives could translate into more market choppiness than we saw in 2024, optimism abounds. This week we’ll get updates on employment and factory orders. And we’ll be looking for continued signs of economic strength and inflation weakness as we move into the new year.

Note: Performance figures for more than one year are annualized. Performance figures for less than one year are cumulative.

Sources:

[1] https://www.investopedia.com/terms/s/santaclauseffect.asp

[2] https://www.cnbc.com/2024/12/30/stock-market-today-live-updates.html

[3] https://www.morningstar.com/bonds/bond-funds-hurt-by-rising-yields-q4-2024

[4]https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_010325.pdf

[5] https://www.noradarealestate.com/blog/stock-market-forecast-for-2025-will-it-soar-or-crash/

[6] https://www.wsj.com/market-data/bonds/benchmarks

This material is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Diversification cannot assure profit or guarantee against loss. There is no guarantee that any investment will achieve its objectives, generate positive returns, or avoid losses. Sequoia Financial Advisors, LLC makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third-parties. Certain assumptions may have been made by these sources in compiling such information, and changes to assumptions may have material impact on the information presented in these materials. Sequoia Financial Advisors, LLC does not provide tax or legal advice.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets