Q1 Market Review – Navigating Market Shifts

by Sequoia Financial Group

by Sequoia Financial Group

Navigating Market Shifts

After two years of exceptional gains, the US equity market entered 2025 with stretched valuations, mainly concentrated in large-cap technology stocks. This created a top-heavy market dominated by the so-called “Magnificent 7” companies—Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. Investor enthusiasm for these high-growth names fueled a momentum-driven rally, but the market’s reliance on this narrow leadership left it vulnerable to disruption. The first quarter of 2025 brought heightened volatility and a sharp correction in US equities, driven by factors such as frothy valuations and policy uncertainty.

Market dynamics have been defined by extreme crowding and narrow leadership, supported by expectations of higher interest rates, optimism surrounding US exceptionalism fueled by advancements in artificial intelligence (AI), and hopes for a pro-growth election outcome. However, recent developments have challenged these narratives. Concerns about a potential economic slowdown, heightened policy uncertainty under the Trump administration, and the disruptive impact of DeepSeek’s cost-efficient AI innovations have emerged as critical factors. These shifts prompt investors to reevaluate growth prospects and market performance assumptions.

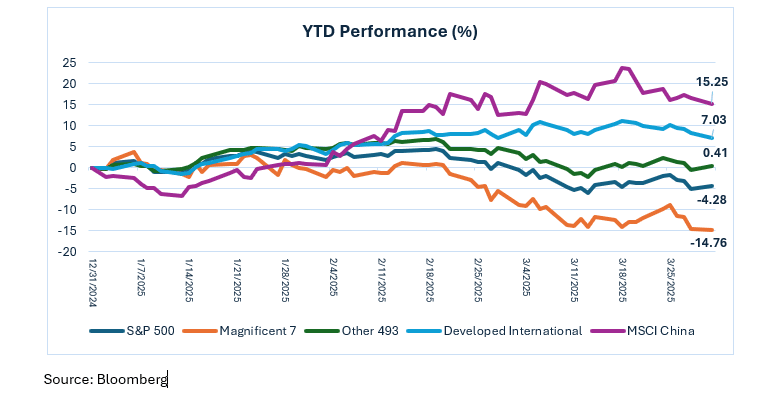

The result was one of the sharpest unwinds of momentum trades in decades, culminating in a 10% correction across major indices. Elevated expectations and challenging year-over-year comparisons for the Magnificent 7 further exacerbated the pullback. Notably, while these tech giants faltered, other market areas showed resilience. For instance, excluding the Magnificent 7, the S&P 500 remained relatively flat amidst uncertainty, while non-U.S. stocks rallied significantly.

This raises an important question: is this rotation away from U.S.-centric tech dominance merely a temporary blip or the beginning of a sustained shift toward value-oriented investments? Early indicators suggest that this rotation may have some staying power. In the following pages, we will explore this potential stylistic shift in market leadership alongside broader themes such as equity corrections, policy uncertainty, economic weakness, and other factors shaping investor sentiment.

The chart above not only shows the concentration of market declines but also illustrates a notable rotation in the market. For example, the S&P 500, excluding the “Magnificent 7,” is marginally positive amidst all the recent uncertainty. Non-US stocks have rallied! This raises the question: Is this just a blip that will ultimately resolve itself with US/Tech supremacy, or is this the story of persistent rotation to value? We suspect that this rotation may have some legs.

In the pages that follow, we will examine the potential stylistic rotation of the market and discuss thoughts about equity market corrections, policy uncertainty, recent economic weakness, and the weather.

Corrections Are Normal

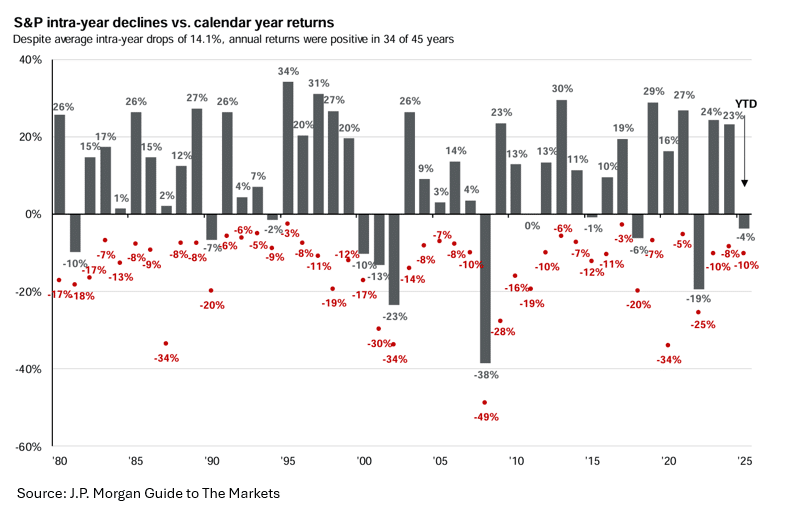

It might be hard to believe, but it was just six weeks ago that the S&P 500 traded to a new all-time high. While often unsettling, market corrections are a normal and healthy part of the equity market cycle. They allow valuations to recalibrate to more sustainable levels, helping reset investor expectations and reduce speculative excesses. The chart below illustrates that the S&P 500 has experienced an average intra-year drawdown of 14.1% over the past 45 years. Despite these periodic pullbacks, annual returns were positive in 34 out of those 45 years—a testament to equity markets’ resilience over time.

These corrections serve as a reminder that short-term volatility is an inherent feature of investing and should be expected as part of the journey toward long-term growth. For disciplined investors, such pullbacks can even present opportunities to reassess portfolios and identify attractive entry points for high-quality assets at more reasonable valuations.

Peak Policy Uncertainty: A Drag on Confidence

Today’s economy faces headwinds, but it is far from a crisis. While confidence has softened compared to a quarter ago, there are no indications of a sharp economic downturn. Recent data has delivered mildly negative surprises, but they do not suggest an imminent credit crisis. Inflation expectations have ticked up slightly, which has weighed on consumer sentiment, but the bond market remains relatively stable. Bonds have played a crucial role as a diversification tool in this environment, with the flight to safety by investors contributing to a decline in long-term rates this year.

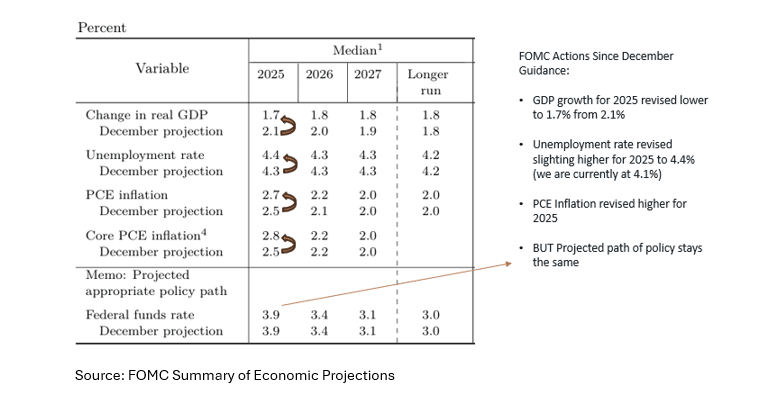

Policy uncertainty has emerged as a significant challenge, impacting sentiment among investors, consumers, and businesses alike. One key concern is the potential implementation of proposed tariffs, which could drag on economic growth while adding to near-term inflationary pressure. Per the chart below, the Fed has adjusted its near-term guidance to reflect the risk of stagflation (lower growth amid higher inflation).

The outlook for economic growth is increasingly tied to the impact of policy uncertainty on business confidence. Late last year, optimism surged as reduced regulations and extended tax incentives were expected to create a pro-business environment, sparking enthusiasm across markets. However, recent developments—particularly aggressive trade policies and tariffs—have dampened this initial optimism. The uncertainty surrounding these policies has left many business leaders hesitant to make major investments.

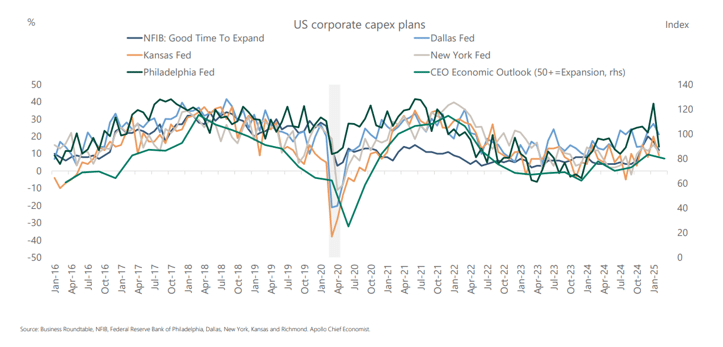

The administration’s tariffs on imports from key trading partners like Mexico, Canada, Europe, and China have disrupted supply chains and clouded the broader economic outlook. This uncertainty has stalled corporate investment plans as businesses wait for clarity on trade rules before committing to significant capital expenditures.

The accompanying chart highlights a sharp decline in planned capital spending, reflecting eroded business confidence. Many corporate leaders are adopting a “wait-and-see” approach, holding off on large-scale investments until they understand the evolving trade landscape. This hesitation underscores how critical clear and consistent policies are for fostering a robust investment climate.

Hopes for a surge in merger-and-acquisition (M&A) activity under a more business-friendly administration have yet to materialize. Instead, lingering uncertainty has weighed on corporate confidence, keeping deal-making subdued. As shown in the chart below, quarterly deal volumes remain well below the optimistic expectations set at the start of the year.

Adding to this cautious environment, the recent tepid reception for CoreWeave—a specialized AI cloud computing company focused on GPU-accelerated infrastructure—has further dampened sentiment around IPO activity. This highlights the broader challenges facing companies looking to tap into public markets amid an uncertain economic and regulatory backdrop

.

The expectation that pro-growth policies would provide strong support for equities seems increasingly out of reach due to the administration’s focus on international trade policy. The so-called “Trump Put”—a perceived safety net for markets—may be less effective than investors had hoped and deeper out of the money than investors may hope. The good news for investors is that markets are already pricing in considerable uncertainty. With time, the fog likely clears, and the pressures on the market ease.

Meanwhile, while monetary policy remains restrictive, the Federal Reserve stands ready to ease monetary policy if economic conditions worsen significantly. However, investors should approach this with caution: history shows that rate cuts often occur alongside deeper economic slowdowns. If the Fed’s rate cuts become more aggressive than anticipated, it could signal a more severe economic contraction. In short, the policy support investors hope for might come with economic stress—be careful what you wish for.

Soft Patch or Recession?

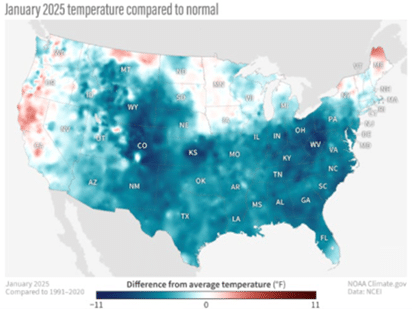

Economic activity in Q1 2025 has been weaker than anticipated, but the US economy is navigating a temporary slowdown rather than heading into a recession. Several factors have contributed to this softness, including a freezing winter, which disrupted consumer spending and skewed year-over-year comparisons. January 2025 marked the coldest January in nearly four decades, with an average temperature of 29.2°F. This weather-driven pause in activity is likely temporary and not indicative of a broader weakening in consumer behavior.

Looking ahead, spending is expected to rebound as temperatures rise and seasonal patterns normalize. Additionally, the late timing of Easter this year (April 20) has shifted a significant portion of Easter-related retail activity into Q2, temporarily distorting quarterly sales comparisons. Historically, about 70% of Easter spending occurs in Q1, but this year’s later date will push more activity into the second quarter. With Easter falling on April 20th this year, this mix is flipped – with only 30% of Easter Activity falling in Q1 and 70% in Q2. Warmer weather and the extended shopping season should provide retailers with opportunities to capture demand for spring-related goods.

Consumer confidence surveys are sending mixed signals, reflecting sharp political divides. However, periods of low consumer confidence have historically created attractive entry points for equity markets. On a positive note, the labor market remains strong, supporting income growth and consumer spending. Wage gains continue to outpace inflation, resulting in positive real wage growth—a key factor in maintaining consumer resilience.

While the data suggests slower growth rather than an outright recession, policy uncertainty remains a significant risk. As we assess how these dynamics evolve in the months ahead, this is a time for cautious monitoring rather than bold predictions.

Regime Change? This Rotation May Have Legs

In Q1 2025, the S&P 500 posted its worst quarterly performance relative to the MSCI World Excluding the US in 16 years, signaling a notable shift in market dynamics. This underperformance coincided with a rotation from growth to value stocks, as US technology companies faced difficult year-over-year comparisons after an extended period of unsustainable growth. At the same time, growth opportunities are beginning to broaden internationally, catching many investors off guard just as sentiment toward non-U.S. markets had reached a low point.

Valuation pressures on US growth stocks have also prompted investors to seek opportunities in sectors and regions with more attractive pricing. International markets, particularly in Europe, benefit from fiscal initiatives such as Germany’s fiscal stimulus package and structural changes in energy and industrial policies. Central banks outside the US are better positioned to ease monetary policy than the Federal Reserve, further supporting international equities.

This rotation could mark the beginning of a longer-term shift in market leadership as investors diversify beyond U.S.-centric high-growth stocks. With improving fundamentals abroad and more attractive valuations, international markets are gaining traction as a compelling area for investment.

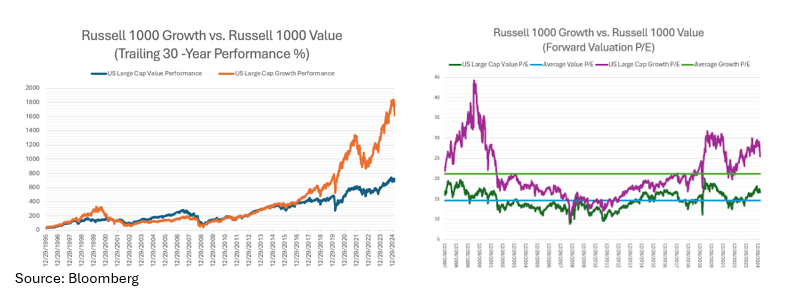

Per the charts below, the 10-year performance gap between Growth and Value is extreme, with US Growth +275% vs. US Value +85%. Further, the valuation gap between value and growth stocks remains wide enough to remain compelling for those looking to diversify away from what’s worked over the last decade.

Conclusion:

The first quarter of 2025 has marked a pivotal moment for global markets, characterized by heightened volatility, policy uncertainty, and a notable shift in market leadership. After years of dominance by US large-cap technology stocks, the so-called “Magnificent 7,” the equity market is undergoing a rotation from growth to value and a broadening of opportunities beyond US borders. The sharp correction in US equities, driven by stretched valuations and challenging year-over-year comparisons, has prompted investors to reassess their strategies and diversify into undervalued sectors and international markets. Notably, while the Magnificent 7 faltered, non-U.S. equities rallied, supported by fiscal initiatives like Germany’s stimulus package and more accommodative monetary policy environments outside the US.

Economic activity in Q1 has been softer than expected, reflecting a temporary slowdown rather than an outright recession. Factors such as an unusually cold winter and the late timing of Easter have distorted consumer spending patterns. Still, these influences will likely fade in the coming months as seasonal trends normalize. Meanwhile, the labor market remains strong, with wage growth outpacing inflation—a positive sign for consumer resilience.

However, policy uncertainty remains a key risk to economic growth and market sentiment. Trade tensions, tariffs, and unclear regulatory policies have weighed on corporate confidence, stalling investment plans and dampening merger-and-acquisition activity. While the Federal Reserve stands ready to ease monetary policy if conditions deteriorate further, history suggests that aggressive rate cuts often coincide with deeper economic slowdowns—a reminder that policy support may come at a cost.

Looking ahead, the ongoing rotation from U.S.-centric growth stocks to value-oriented and international investments could signal a longer-term regime change in market dynamics. With valuation gaps between growth and value stocks at historical extremes and improving fundamentals abroad, international markets present compelling opportunities for diversification. While challenges remain, disciplined investors who adapt to these shifts may find attractive entry points as markets recalibrate. As always, navigating this environment will require careful monitoring and focusing on long-term objectives amid short-term volatility.

As always, we look forward to working closely with you in the coming year to help you achieve your financial goals and secure your financial future. Thank you once again for your valued relationship. Here’s to a bright and successful 2025!

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets