The third quarter of 2024 was a period of heightened volatility for investors, marked by significant shifts in market dynamics, evolving economic conditions, the looming influence of geopolitical factors, and the unique challenges of a contentious U.S. election year. This comprehensive review explores the key trends, challenges, and opportunities that defined the quarter.

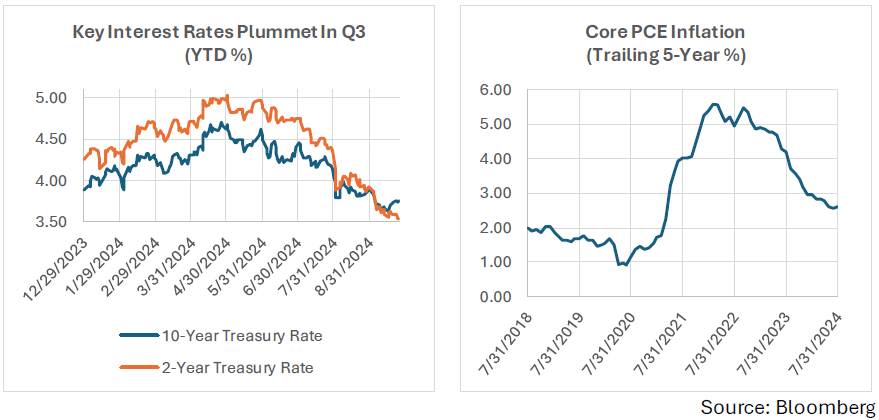

Q3 2024 featured a significant shift in interest rate expectations, which profoundly impacted market dynamics. As illustrated in the accompanying chart, we observed a substantial decline in interest rates across various maturities. This downward trend in Treasury yields can be attributed to several factors: Firstly, market participants began anticipating a more accommodative stance from the Federal Reserve. The expectation of a dovish policy shift naturally exerted downward pressure on Treasury yields. Secondly, the changing Fed posture is driven by signs of economic softening, particularly evident in the labor market. Recent data suggests a moderation in employment growth and wage pressures, potentially cooling the previously overheated job market.

Lastly, near-term inflation indicators are pointing towards a resumption of disinflationary trends. This development has bolstered confidence that inflation may return to the Federal Reserve’s 2% target. These factors collectively contributed to the notable decline in interest rates and have prompted a reevaluation of investment strategies across various asset classes.

The catalyst for this shift was the release of June’s Consumer Price Index data on July 11, 2024, which came in lower than anticipated. This development and subsequent labor market data have substantially changed interest rate policy expectations and equity market dynamics. The June CPI data gave policymakers increased confidence that inflation was moving towards the Federal Reserve’s 2% target. This shift in the balance of risks, favoring concerns over weaker growth rather than higher inflation, set the stage for a pivotal market moment. All eyes then turned to the labor market as a critical indicator of U.S. consumer health, the backbone of our resilient economy.

The catalyst for this shift was the release of June’s Consumer Price Index data on July 11, 2024, which came in lower than anticipated. This development and subsequent labor market data have substantially changed interest rate policy expectations and equity market dynamics. The June CPI data gave policymakers increased confidence that inflation was moving towards the Federal Reserve’s 2% target. This shift in the balance of risks, favoring concerns over weaker growth rather than higher inflation, set the stage for a pivotal market moment. All eyes then turned to the labor market as a critical indicator of U.S. consumer health, the backbone of our resilient economy.

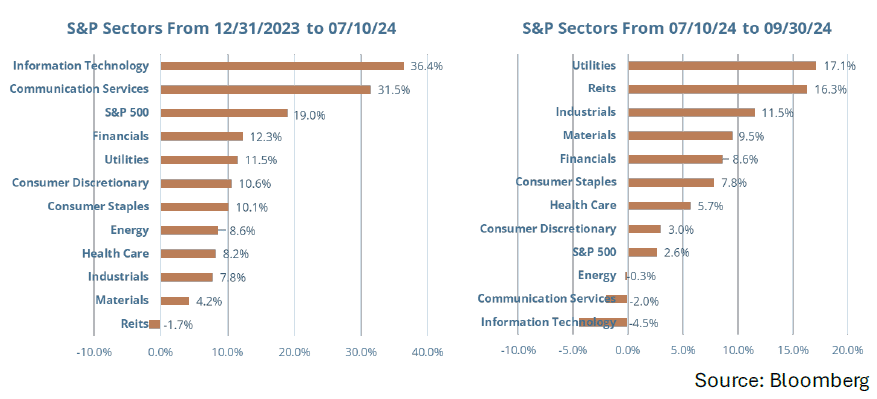

July’s labor market data shocked the system. Payroll growth fell short of expectations, and the unemployment rate surprised to the upside, igniting fears of an economic slowdown. These developments have prompted a notable change in policymakers’ stance, leading to significant shifts in interest rate expectations and equity market leadership. The technology sector, long the market’s dominant source of earnings growth, began to underperform in the third quarter.

After an extended period of outperformance, many tech stocks had reached elevated valuations, prompting some investors to reconsider their positions and seek opportunities elsewhere. Conversely, more defensive and interest rate-sensitive sectors have found renewed favor in this changing environment. Companies with robust current cash flows and more modest valuations have attracted increased attention from investors seeking stability and reliable returns.

The appeal of value stocks has been further enhanced by their often higher dividend yields, which have become more attractive relative to fixed-income alternatives in a potentially lower-interest-rate environment. Furthermore, value sectors closely tied to broader economic performance have seen a surge in interest as investors position themselves for a more accommodative monetary policy stance. This shift in market leadership reflects the complex interplay between economic indicators, policy decisions, and investor sentiment.

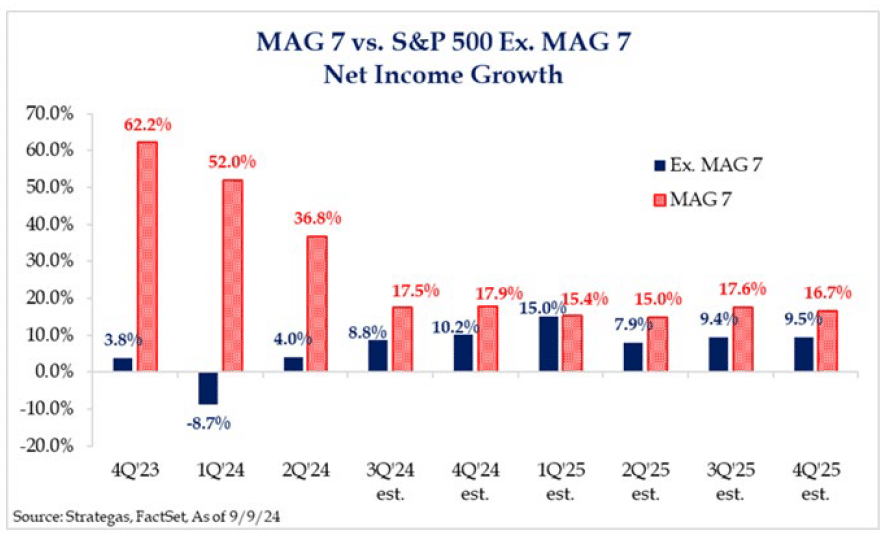

Notably, The U.S. stock market continues to demonstrate resilience, reaching new peaks despite underlying changes in sector dynamics. The S&P 500 resumed its upward momentum without the leadership of the “Magnificent Seven.” This evolving landscape has led to a more balanced distribution of market performance across various sectors, reducing the previously observed concentration. Such diversification is generally viewed as a positive development for overall market health. Additionally, earnings trends reflect this shift; previously, earnings growth was primarily confined to a select few sectors, but recent data indicates a more equitable distribution across different industries.

As earnings growth becomes more evenly spread, it is expected to contribute to a broader breadth of market performance. This trend could foster a more robust and diverse market environment, ultimately decreasing reliance on a few high-performing sectors to sustain overall growth.

These developments underscore the importance of maintaining a diversified portfolio and the need for investors to remain adaptable in response to macroeconomic changes. They also highlight that periods of economic transition can create opportunities across various sectors and investment styles rather than favoring a single approach.

Economic Activity is Normalizing, Not Plummeting

The post-pandemic economic landscape has been characterized by a gradual normalization of consumer behavior, with spending patterns diverging from trends observed during the height of COVID-19. As the economy decelerates from the post-pandemic surge in activity, investors have become increasingly sensitive to macroeconomic data, leading to heightened volatility in financial markets. While acknowledging this deceleration, it is essential to recognize that these trends represent a return to pre-pandemic norms rather than a cause for significant concern.

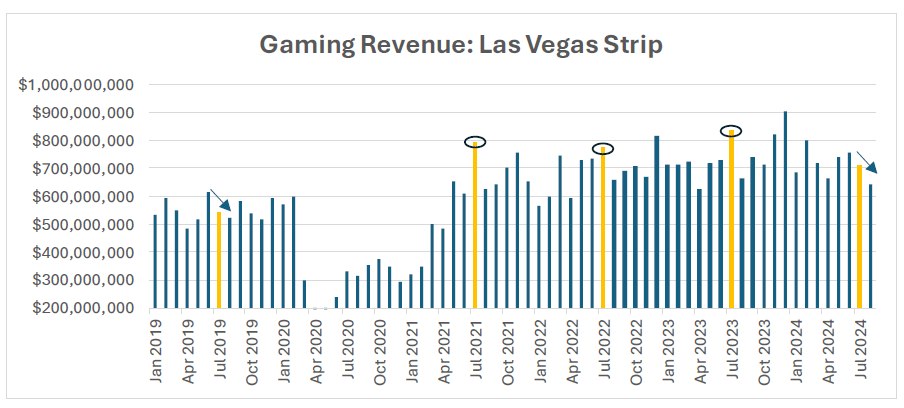

For example, this normalization is particularly evident in the travel and entertainment sectors, as exemplified by recent developments in Las Vegas. The city, often regarded as a bellwether for discretionary spending, has experienced a year-over-year decline in summer tourism and gambling revenue. However, this should not be interpreted as a dramatic downturn but rather as a reemergence of typical seasonal patterns. Historically, Las Vegas has experienced slower periods during the summer months, and the return of these seasonal fluctuations indicates a shift toward pre-pandemic norms.

Source: LVSTATS

It is crucial to note that this trend is not unique to Las Vegas but reflects a broader shift in consumer priorities and spending habits across various tourist destinations that initially experienced a post-lockdown boom. We observe similar trends in theme park visitations and forward bookings for golf resorts and cruises. As the economy stabilizes, these patterns are anticipated to further align with historical norms, signaling a return to more predictable consumer behavior and economic cycles.

As the economy transitions from the extraordinary measures implemented during the pandemic, consumer spending patterns are expected to evolve significantly. The robust consumer activity that has been a cornerstone of economic growth will increasingly rely on conventional income sources rather than pandemic-era stimulus. Since consumer spending accounts for approximately 70% of U.S. GDP growth, the labor market’s health will play a crucial role in sustaining income growth and spending power. Simultaneously, asset value fluctuations, including equities and real estate, will significantly impact consumer confidence and expenditure decisions. These factors combined will shape the trajectory of consumer behavior and its contribution to overall economic performance in the post-pandemic landscape.

As we move further from the acute phase of the pandemic, normal business seasonality is likely to reassert itself, and consumer behavior will continue to normalize. While economic data may appear softer compared to recent years’ heightened activity, investors should exercise caution in their interpretations, recognizing that this normalization process is a natural part of the economic cycle rather than a cause for alarm. This nuanced understanding of the evolving economic landscape will be essential for making informed decisions in the post-pandemic era.

The Cutting Cycle Has Begun—The Fed Put Is Back in Play

“We do not think we are behind, but you can take this as a sign of our commitment to not get behind.”

–Jay Powell (09/18/24)

Since the Federal Reserve’s meeting in June, the economic landscape has shifted notably, leading to significant actions during their recent September gathering. The inflation outlook has improved, with moderating price pressures, while the labor market has shown signs of softening, marked by a concerning rise in unemployment. These developments prompted the Fed to take decisive action, initiating a rate-cutting cycle with an unexpected 50 basis point reduction—double the usual increment. This was the most important message from the Fed during this meeting, signaling a clear shift in focus from controlling inflation to safeguarding the labor market and supporting economic expansion.

The Fed’s decision reflects a new urgency to normalize monetary policy quickly to prevent further deterioration in employment conditions. By opting for a more significant cut, the central bank aims to avoid the pitfalls of maintaining an overly restrictive stance that could lead to a policy-induced recession, a common risk associated with historical monetary policy errors. Chair Jerome Powell’s statement, “We do not think we are behind, but you can take this as a sign of our commitment to not get behind,” underscores this proactive approach and highlights their intention to learn from past mistakes.

The Fed acknowledges its vulnerability to policy errors due to reliance on lagging data—akin to driving while looking in the rearview mirror—which can lead to financial missteps. This recent rate cut marks the first reduction in more than four years and serves as a psychological signal of decisiveness and confidence from the Fed. It indicates a willingness to anticipate economic challenges rather than waiting for them to manifest before acting. As such, this meeting represents a pivotal moment in the Fed’s strategy, emphasizing its commitment to fostering stability and avoiding potential economic pitfalls in the coming months. The forward-looking approach to policy increases the likelihood of achieving a soft economic landing.

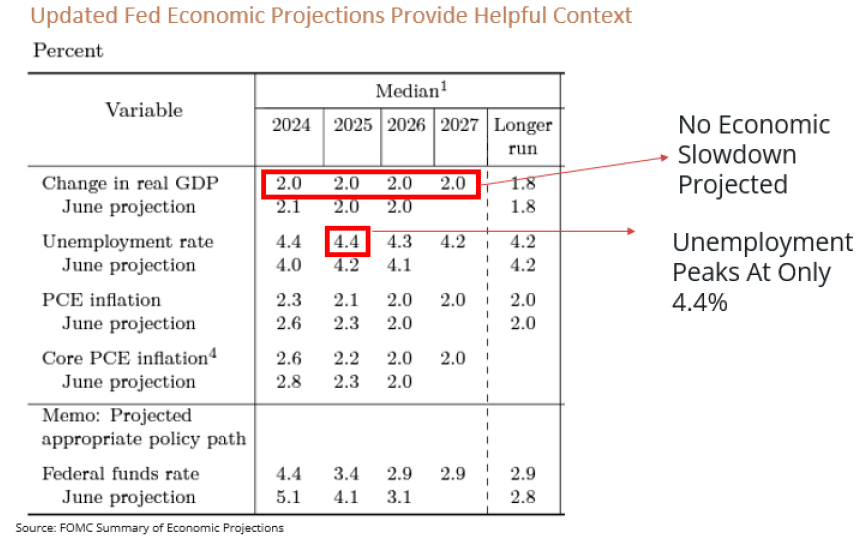

The Federal Reserve’s recent decision to cut interest rates was accompanied by its updated Summary of Economic Projections, offering valuable insights into the central bank’s outlook for the coming years. These projections paint a picture of a “soft landing” scenario for the U.S. economy, with real GDP growth expected to maintain a healthy 2% pace through 2027. This stable growth forecast suggests that the Fed’s current trajectory for interest rates is predicated on a relatively optimistic economic outlook. Notably, the projections indicate that the unemployment rate is anticipated to peak at a modest 4.4%, considered relatively low by historical standards.

The Fed’s current rate path and economic projections are particularly significant as they do not factor in any substantial economic downturn. The implication is that if economic conditions were to deteriorate more than expected, the central bank might need to accelerate its rate-cutting cycle or implement more aggressive monetary easing measures. The Fed’s projections provide a baseline scenario, with the understanding that any significant deviation from this outlook could prompt a more rapid or extensive policy response.

This forward-looking approach by the Fed demonstrates its readiness to adapt quickly to changing economic circumstances. By presenting a scenario that doesn’t account for economic deterioration, the Fed effectively signals its commitment to maintaining economic stability and its willingness to take more decisive action if necessary. This nuanced perspective underscores the delicate balance the Fed is attempting to strike between supporting economic growth and maintaining price stability in an uncertain economic environment.

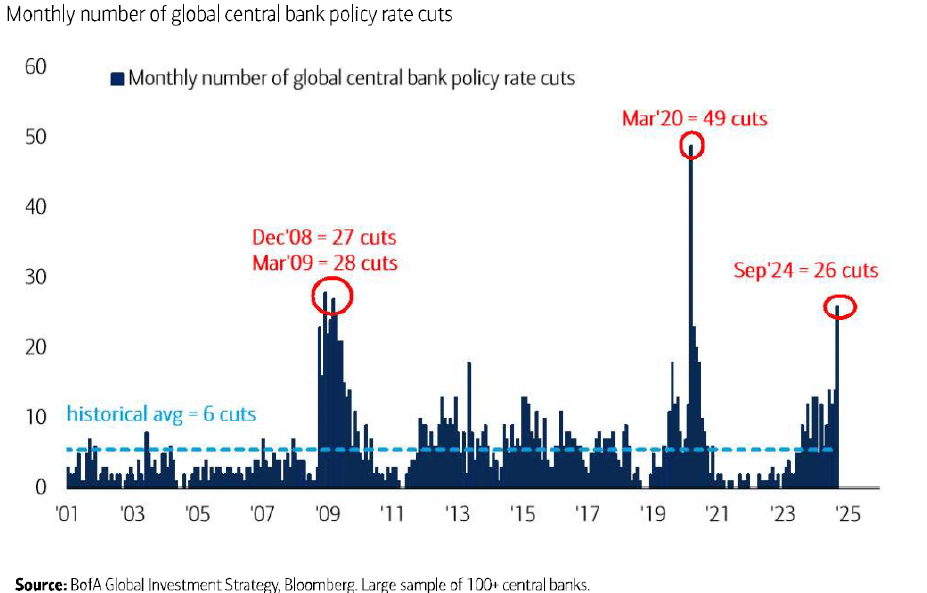

The Federal Reserve’s decision to ease monetary policy has significant ripple effects across the global financial landscape, particularly in providing other central banks with increased flexibility in their policy decisions. China’s recent policy actions serve as a prime example of this dynamic. Following the Fed’s rate cut, Chinese policymakers have dramatically shifted their approach from modest, inconsistent interventions to a more robust and comprehensive strategy. This change in stance suggests a transition from a cautious, incremental approach to something akin to a government guarantee for economic stability or even a “whatever it takes” mentality reminiscent of bold central bank actions during past crises.

This newfound policy aggressiveness in China is directly enabled by the Fed’s easing, which has created a more accommodative global financial environment. Previously, there was a perception that Chinese authorities were willing to allow the deflation of the real estate bubble to rebalance the economy towards other sectors. However, recent statements and actions indicate a growing recognition of the deflationary risks posed by this approach. Policymakers are now explicitly calling for stability in property prices, acknowledging the crucial role of the real estate sector in maintaining consumer and business confidence. This pivot represents a significant change in China’s economic strategy, marking the beginning of a more proactive and interventionist phase in its economic management. The coordinated and substantial nature of these recent policy moves suggests that Chinese authorities are now fully committed to stemming the tide of economic slowdown and rekindling growth across various sectors of the economy.

Moreover, the ripple effects of the Fed’s easing extend beyond China; September 2024 marked the biggest month for central bank policy cuts this century, highlighting how interconnected global monetary policies are and underscoring the significant influence of the Federal Reserve’s decisions on the international financial landscape.

Final Thoughts Heading into The US Presidential Election

As we find ourselves in the midst of an intense political season, both major candidates are focusing their rhetoric on tax policies, vying for voter attention with promises of reform and relief. However, this narrow focus obscures a more pressing issue that neither seems eager to address: the problem of government spending. The elephant in the room remains the ballooning deficit, which continues to grow unchecked. This reluctance to confront spending head-on raises questions about what will transpire after the November 3rd election. Will the stark reality of the deficit and its far-reaching consequences finally come into sharper focus once the campaign promises fade?

There’s a growing concern among economists and policy experts that without addressing the spending side of the equation, any tax policy changes will be insufficient to tackle the long-term fiscal challenges facing the nation. The post-election period may force a reckoning with these issues, as the newly elected administration will need to grapple with the economic realities beyond campaign trail rhetoric.

Conclusion—Recession Odds Lower, Growth Opportunities Broadening Out

In conclusion, the third quarter of 2024 has been marked by significant volatility and shifting dynamics in the financial markets, primarily driven by changes in interest rate expectations and economic indicators. The Federal Reserve’s proactive decision to cut interest rates by 50 basis points reflects a commitment to fostering economic stability amid signs of softening in the labor market and inflation trends moving toward their target. This strategic pivot not only signals a desire to avoid potential economic pitfalls but also provides other central banks, such as China’s, with the flexibility to implement more aggressive policy measures.

Q324 witnessed a notable shift in market leadership, with technology stocks underperforming after an extended period of dominance while more defensive and interest rate-sensitive sectors gained favor. This rebalancing has led to a more equitable distribution of market performance and earnings growth across various industries, potentially fostering a healthier and more diverse market environment.

Consumer behavior continues to normalize post-pandemic, with spending patterns in sectors like travel and entertainment returning to more predictable seasonal trends. While this normalization may appear as a slowdown compared to recent years, it represents a return to pre-pandemic norms rather than a cause for alarm.

The Fed’s updated economic projections suggest a “soft landing” scenario, with stable GDP growth and modest unemployment rates projected through 2027. However, these projections also imply a readiness to take more aggressive action should economic conditions deteriorate beyond current expectations.

As global economic conditions evolve, maintaining discipline in portfolio construction becomes increasingly crucial. Investors should resist the temptation to avoid areas of the market currently out of favor, such as small-cap or international stocks. Instead, a balanced and diversified approach remains essential for navigating this complex landscape. The interplay between monetary policy, economic indicators, and market dynamics will continue to shape the investment landscape, requiring investors to remain vigilant and adaptable to capitalize on opportunities across various sectors in the months ahead.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets