Q4 Market Review – The US Economy Continues To Defy Expectations

by Sequoia Financial Group

by Sequoia Financial Group

Where The Growth Is…

The US economy continues to surpass expectations of a slowdown in recent years, with 2024 proving no exception. Despite facing challenges such as uncertainty surrounding a presidential election, high interest rates, and a cooling labor market, economic growth remained robust throughout the year. The growth rate of the US economy doubled expectations coming into the year. As we head into 2025, the investment world is experiencing a post-election wave of optimism, with investors displaying a strong risk appetite driven by fear of missing out rather than concern over potential downturns. This shift has led to complacency, with market participants overlooking typical risk factors. The market’s upward momentum is creating a self-reinforcing cycle, attracting more buyers and pushing valuations higher.

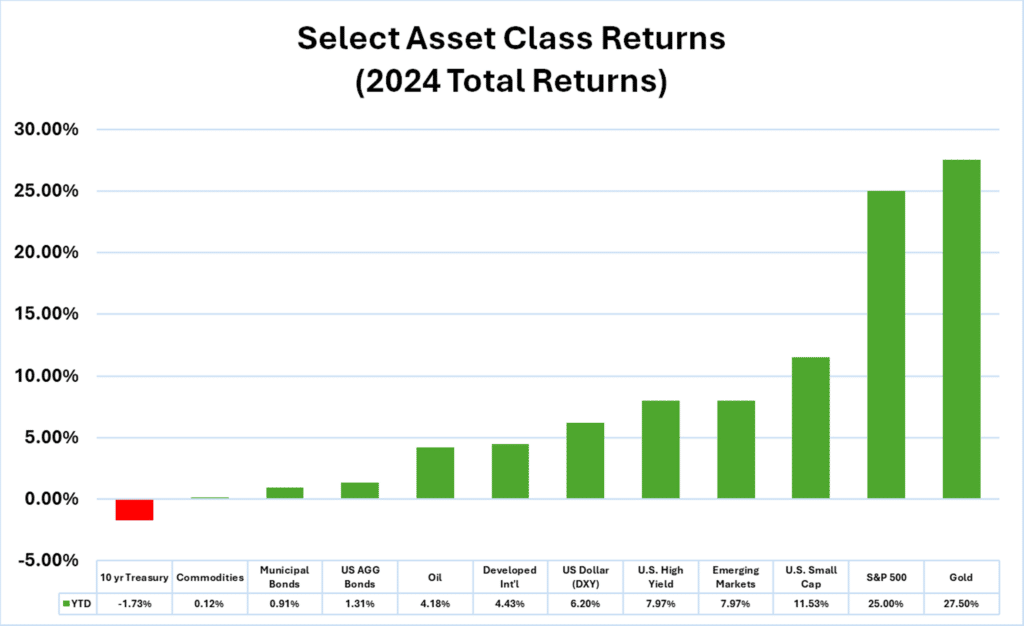

As we reflect on the market’s performance over the past two years, it’s clear that the S&P 500 has demonstrated remarkable resilience. After a robust 24% gain in 2023, the index continued its upward trajectory with a 25% increase in 2024, marking one of the most substantial back-to-back periods in market history. This impressive performance came despite numerous challenges, including the aftermath of the 2021 Tech Bubble, a Regional Bank Crisis, heightened geopolitical tensions, deglobalization trends, and global political uncertainty. US stocks have steadily climbed a metaphorical wall of worry for two years.

As we approach 2025, financial markets are grappling with a confluence of concerns that are shaping investor sentiment and economic outlooks. The return of a Trump administration has introduced significant policy unpredictability, while worries about economic growth outside the United States are mounting. The persistently high interest rate environment pressures various sectors, influencing borrowing costs and corporate profits. The heavy reliance on a few high-performing tech giants has also raised questions about concentration risk and overall market health. These factors collectively contribute to a complex and uncertain market environment, with investors carefully weighing risks and opportunities in this evolving landscape.

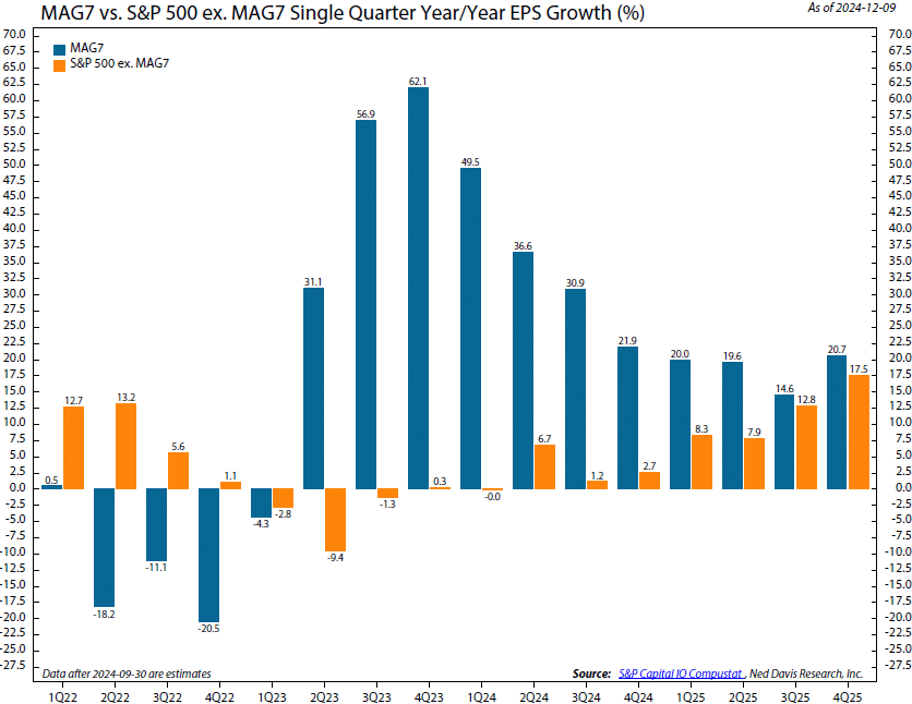

Risk assets performed well in 2024 as recession concerns diminished throughout the year. US growth stocks led global equities, supported by their dominant earnings profile and a strong US dollar. Despite expectations of modest gains following the previous year’s surge, driven by artificial intelligence (AI) investments and economic resilience, the S&P 500 continued to set new records throughout the year, gaining 25% in 2024. The biggest US companies have outperformed the index for a good reason – they have generated much more substantial profit growth. The chart above illustrates earnings growth dispersion between the largest growth names in the index and the remaining 493 companies.

This remarkable performance capped the most substantial two-year run since the late 1990s dot-com era, surpassing expectations that Treasuries might outperform equities as the Federal Reserve shifted towards rate cuts. In the fixed-income space, our strategy of favoring credit exposure over duration proved advantageous. Higher coupon payments and tightening credit spreads more than compensated for the gradual rise in government bond yields.

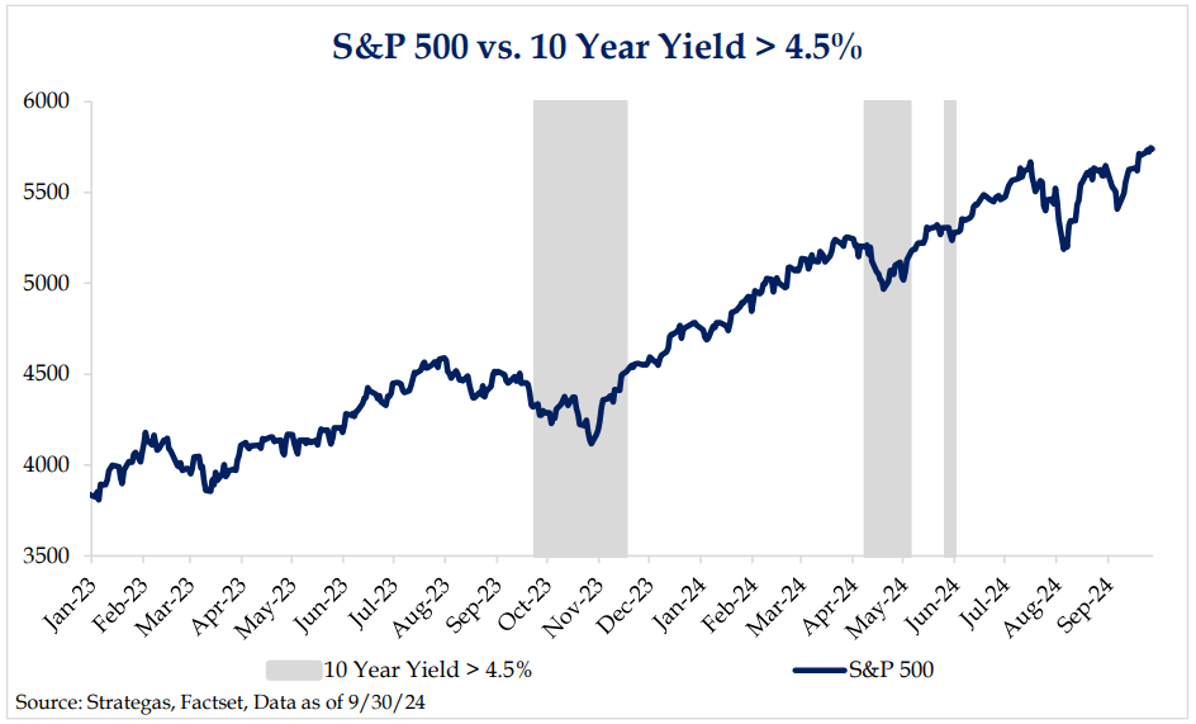

Our fixed-income portfolios, positioned with relatively short duration and increased credit exposure, performed well in this environment. The portfolio maintains an A rating with an average duration of approximately 3.8 years and offers a yield to maturity of ~7.0%. As the 10-year US Treasury yield has climbed above 4.5%, we are becoming more receptive to additional interest rate risk in our fixed income allocation. However, we remain cautious about the recent compression of high-yield spreads, which have narrowed considerably. This development warrants careful consideration in our ongoing portfolio management and risk assessment.

Source: Bloomberg

There are numerous positive factors supporting market enthusiasm. The macroeconomic environment is favorable, with a strong labor market, positive real wage growth, and a robust wealth effect bolstering consumer confidence. The policy landscape is also supportive, featuring less restrictive monetary policy, expansionary fiscal measures, and regulatory easing. Additionally, the earnings outlook appears promising, with achievable growth projections and potential AI-driven productivity gains. While current valuations suggest future returns may align closely with earnings growth, market momentum remains strong, with broad gains across major indices. Furthermore, the potential reallocation of substantial cash reserves from lower-yielding instruments to equities could provide additional support for stock prices as interest rates decrease.

While commodities broadly underperformed, Gold and Bitcoin, both alternatives to traditional fiat currency, rallied significantly in 2024. Gold is heading for one of its most significant annual gains this century, with a 27% advance fueled by US monetary easing, sustained geopolitical risks, and a wave of purchases by central banks. Meanwhile, Bitcoin, which many consider the digital version of the yellow metal, rallied over 125% in 2024. This remarkable performance of gold and Bitcoin underscored their appeal as hedges against inflation and global economic uncertainties, outpacing traditional benchmarks and attracting increased investor interest.

However, this bullish environment raises questions about potential disruptors to the prevailing mood. It is crucial to consider factors that might trigger a shift in market sentiment or cause investors to become more wary of downside risks. While current sentiment is positive, prudent investors should remain vigilant, balancing optimism with realistic risk assessment in this evolving landscape.

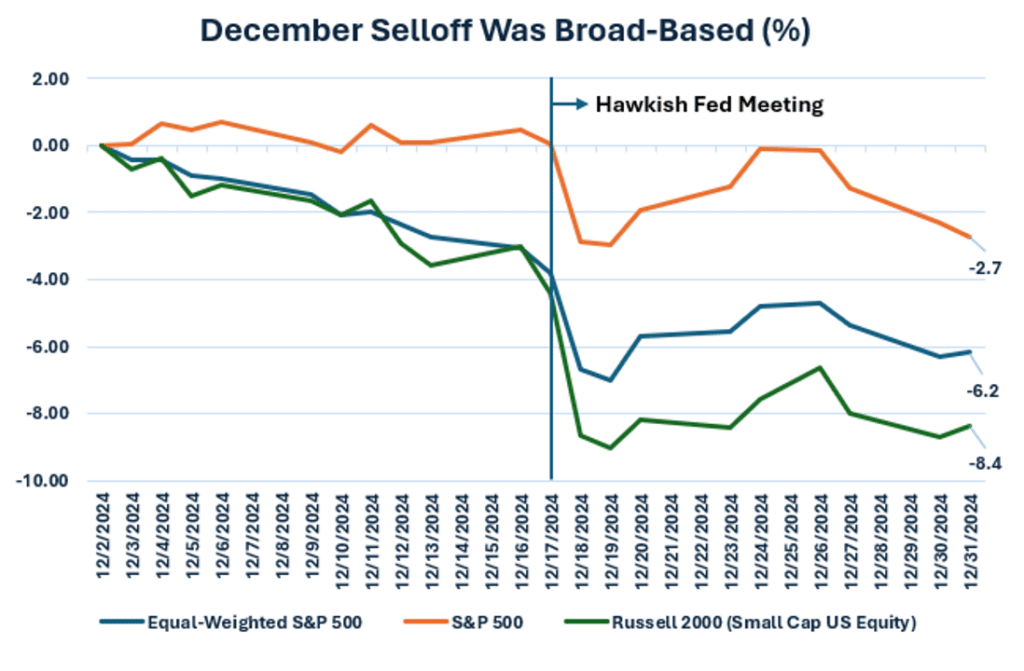

As a reminder of the stock market’s downside volatility, US equities experienced a notable broad-based selloff in December. While the market-cap-weighted version of the S&P 500 declined by only 2.7% (with losses buffered by the largest stocks in the index), the equally weighted version declined by 6.2%. Furthermore, small-cap US stocks fell 8.4% in the year’s final month.

Source: Bloomberg

As we reflect on December’s market dynamics, it’s clear that interest rate policy continues to play a pivotal role in shaping market concentration. Earlier in 2024, we observed a broadening of gains beyond the so-called Magnificent Seven, the largest and fastest-growing segment of the market, as expectations of lower interest rates took hold. However, recent developments have altered this trajectory. Persistently high inflation has prompted the Federal Reserve to adopt a more hawkish stance, signaling that rates may remain elevated for an extended period. This shift in rate expectations has led to a reconcentration of market gains. Notably, the top 10 largest stocks in the index now account for an unprecedented 39% of the market’s total value, underscoring the significant impact of monetary policy on market structure and performance.

Weight Of The Top 10 Stocks In The S&P 500

Source: JP Morgan Guide To The Markets

Inflation Still the Boogeyman

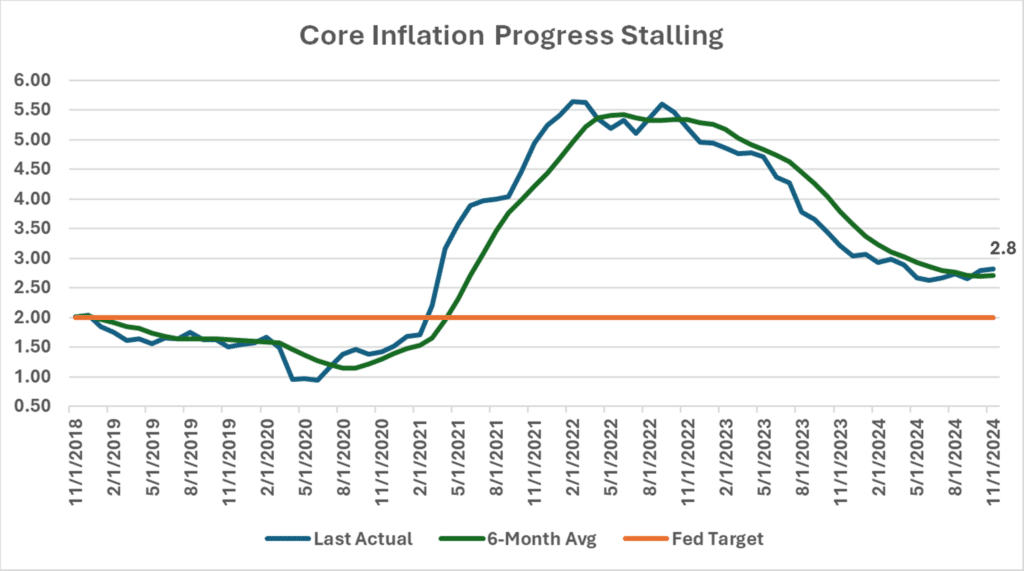

Inflation continues to be the primary factor dampening market sentiment. In the most recent Federal Reserve meeting, despite a reduction in policy rates, Jerome Powell, the Fed Chairman, maintained a hawkish tone. The Federal Open Market Committee (FOMC) significantly revised its outlook on the pace of potential rate reductions compared to their previous meeting in September. This shift in stance is attributed to inflation’s persistence, which has not abated as quickly as policymakers had anticipated.

Source: Bloomberg

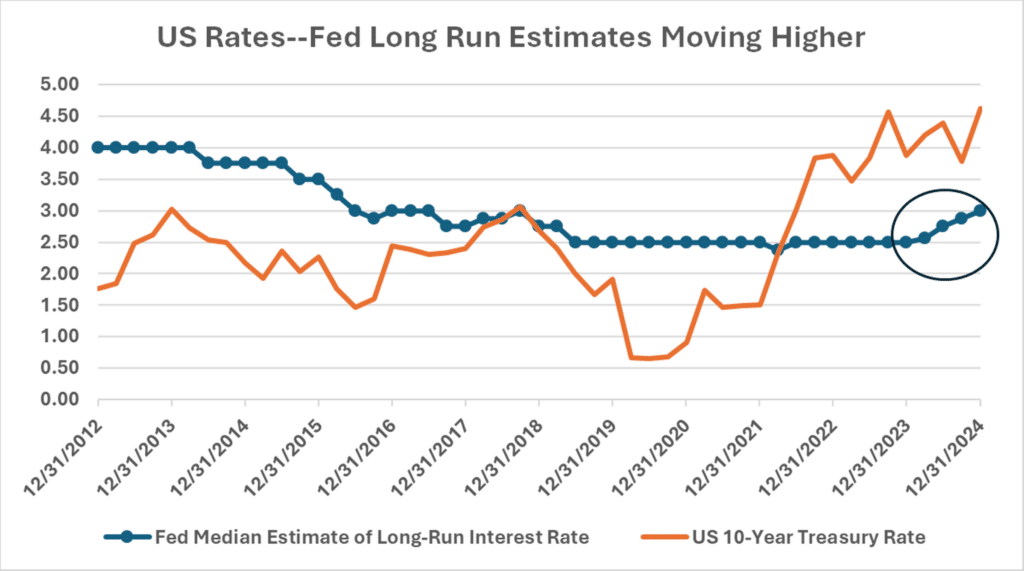

As a result, The Federal Reserve has extended its timeline for achieving the 2% inflation target to 2027, signaling a prolonged period of higher policy rates. This adjustment underscores policymakers’ complex challenge of balancing inflation control with economic growth support. The Fed has also revised its long-term Fed Funds rate estimate upward, indicating a less dovish stance than markets anticipated. This shift is evident in the evolving median estimates of FOMC members, which steadily increased throughout 2024, pushing 10-year rates near 20-year highs.

In 2025, Federal Reserve Chair Jerome Powell faces a delicate balancing act amid increased uncertainty surrounding fiscal policy measures. The Fed’s recent hawkish stance may be a response to potential inflationary pressures arising from the incoming Trump administration’s policies. Powell must navigate this complex landscape while maintaining a non-confrontational stance toward the President-elect.

The Fed has adjusted its inflation projections upward, expecting core inflation to reach 2.5% next year, up from their previous estimate of 2.2%. Notably, 15 of 19 Fed officials now see a risk of inflation exceeding their forecast, a significant increase from just three in September. These revisions may anticipate potentially inflationary fiscal initiatives under the new administration, highlighting the ongoing recalibration of monetary policy in response to persistent inflationary pressures and changing economic dynamics.

Source: Bloomberg

Entering 2025 In Danger Zone for Rates & The Market

Market drawdowns have primarily occurred when the 10-year US Treasury yield surpassed 4.5%. Given persistent inflation and substantial government debt loads, the prospect of a “higher for longer” rate environment seems increasingly likely as we look ahead.

This scenario has broad implications for the market:

- Equity market valuations are under pressure when rates exceed 4.5%.

- The potential for market gains to broaden out is limited if rates remain elevated.

- Small-cap stocks require lower rates to drive earnings acceleration.

Without a decrease in interest rates, it’s challenging to envision a market environment characterized by more broadly diversified gains. The performance concentration among large-cap stocks may persist, as they have demonstrated more robust profit growth in the face of higher rates.

This interest rate sensitivity underscores the delicate balance between monetary policy and market performance. As the Federal Reserve navigates the complex task of managing inflation while supporting economic growth, investors must remain vigilant to the potential impacts of sustained high rates on different market segments.

The Elusive American Dream

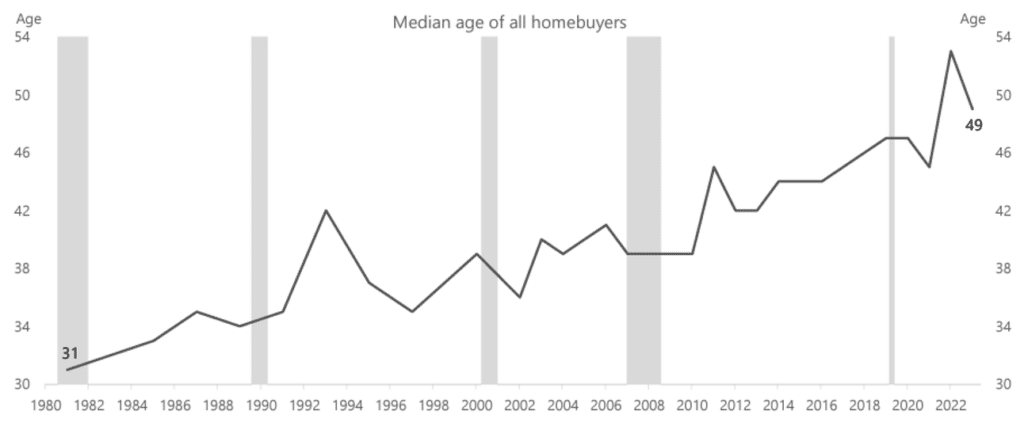

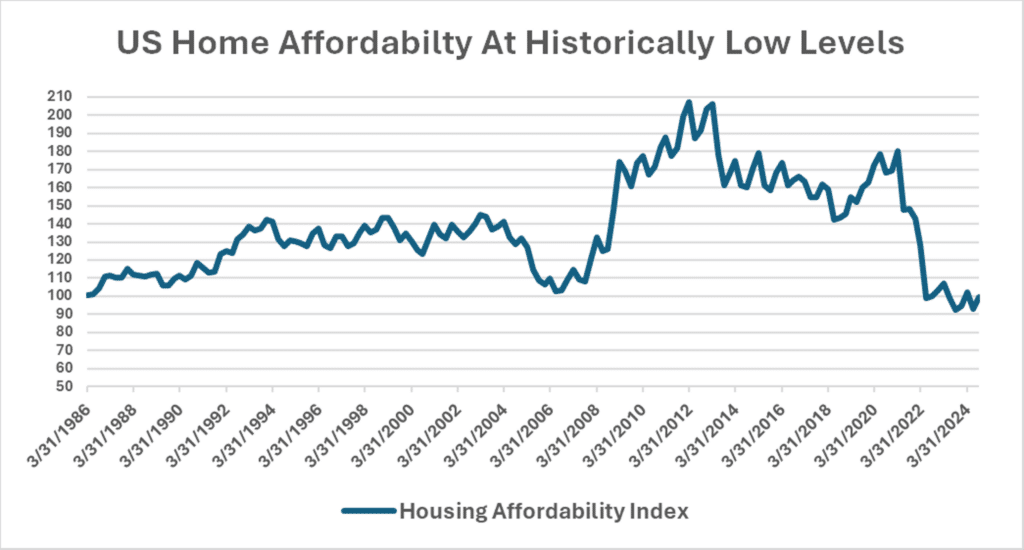

The American dream of homeownership has become increasingly elusive. The median age of homebuyers rose dramatically from 31 in 1981 to 49 today, reflecting the growing challenges aspiring homeowners face. US home affordability has plummeted to historically low levels, with only 16% of homes on the market considered affordable in 2023, compared to 50% a decade ago.

The median age of all homebuyers is now 49 years old, up from 31 in 1981

The housing market continued to face challenges in 2024 due to elevated borrowing costs, with mortgage rates approaching 7% again as expectations grew that the Federal Reserve would delay interest rate cuts. These high rates have nearly doubled typical monthly payments in three years, stretching household budgets to their limits. To attract buyers in this challenging environment, contractors offered incentives such as mortgage buydowns and payment assistance. However, home sales remained below pre-pandemic levels, with the National Association of Realtors projecting that the 2024 sales pace would fall even lower than the previous year, which had already marked the worst performance since 1995. This situation is not only delaying homeownership for many but also potentially widening the wealth gap between homeowners and renters as the dream of owning a home slips further away for a growing population segment.

Source: Bloomberg

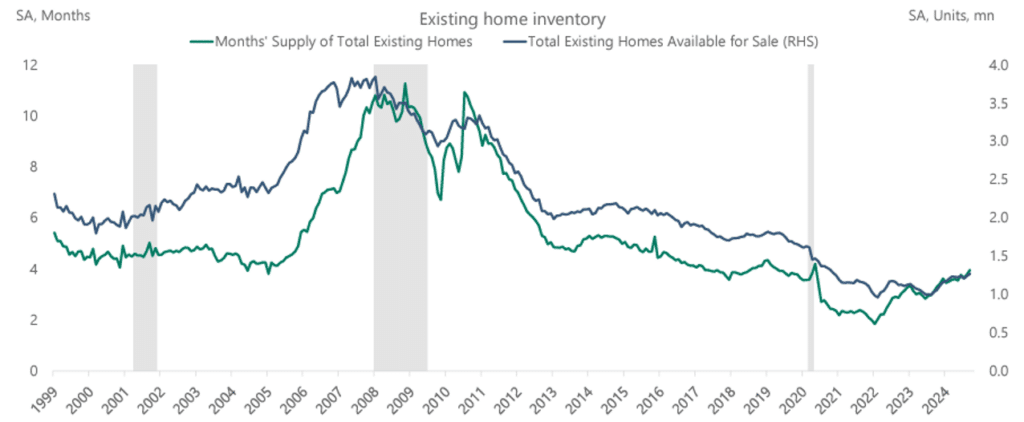

The U.S. housing market continues to grapple with a significant shortage of homes, exacerbating affordability issues and limiting options for potential buyers. As of Q3 2024, the national housing shortage is estimated at 3.7 million units, only slightly improved from the 3.8 million unit deficit in Q4 2020. This persistent undersupply is driven by several factors, including construction delays, high building costs, and the “lock-in effect” keeping homeowners with low-interest mortgages from selling. This scarcity has contributed to rising home prices and intensified competition among buyers, with the months’ supply of existing homes at 4.3 months in September 2024, well below the 5 to 6 months typically considered indicative of a balanced market.

Source: NAR/Apollo

The resilience of consumer spending in the current economic climate presents a nuanced picture, with a stark contrast between lower-income and higher-income consumers. While rising prices have pressured lower-income households, the higher-end consumer drives overall spending. This dynamic is significant, given that the top 40% of income earners in the US account for 65% of total consumer expenditure.

The “wealth effect” has been crucial in sustaining spending habits among higher-income consumers. This economic phenomenon, where increased asset values boost consumer confidence and spending, has been particularly evident as stock markets and home prices have risen. Higher-income earners, more likely to own such assets, have felt more financially secure, leading to maintained or increased spending despite unchanged incomes or fixed costs.

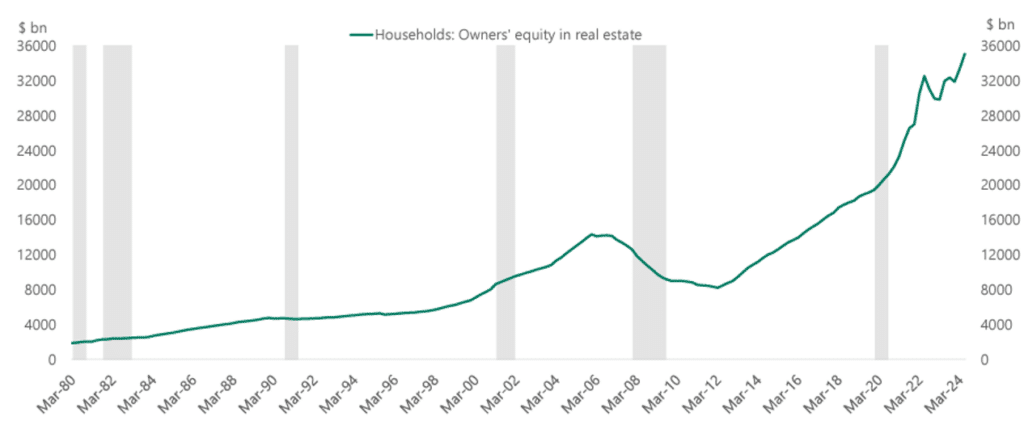

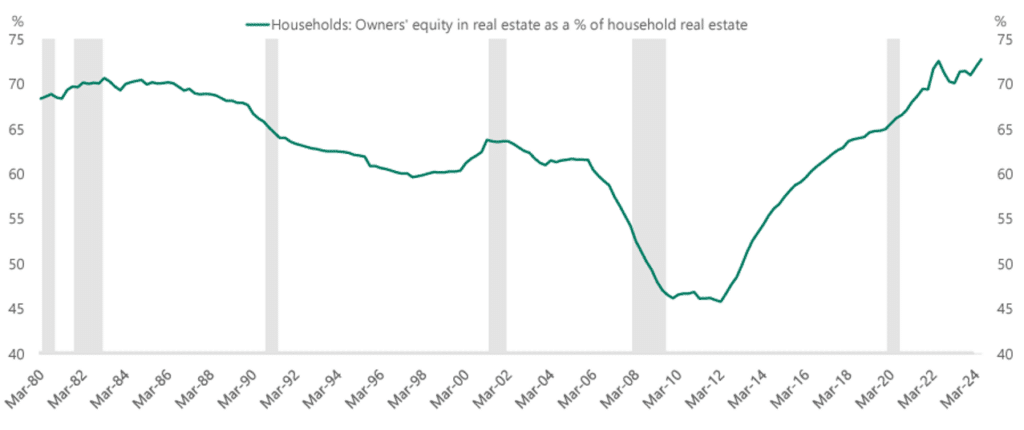

Recent data shows that the housing market’s influence on consumer confidence, particularly among homeowners, is strikingly evident. Homeowners’ equity has reached an unprecedented $35 trillion, reflecting a substantial increase in property values nationwide. Concurrently, the proportion of equity held in American homes has climbed to a record-high 73%. These figures underscore the significant wealth effect generated by the housing market, potentially boosting spending confidence among homeowners. However, it’s crucial to note that this data primarily reflects the financial position of existing homeowners, not accounting for the challenges faced by non-homeowners or aspiring buyers in the current market.

Households’ equity in real estate rising to $35trn

Source: NAR/Apollo

Households’ equity share in real estate is at all-time high of 73%

Source: NAR/Apollo

However, this asset price sensitivity is a double-edged sword. While it has supported consumer confidence and spending during periods of asset appreciation, it also exposes the economy to potential downturns. A significant drop in asset prices could trigger a negative wealth effect, potentially leading to a sharp contraction in consumer spending, especially among the higher-income segment driving economic growth. This vulnerability underscores the delicate balance in the current economic landscape and the potential risks to consumer spending and broader economic stability should asset values decline.

Conclusion:

As we look ahead to 2025, equity and fixed-income markets present evolving opportunities amidst a complex economic landscape. While the final stages of inflation reduction may prove challenging, we anticipate that ongoing monetary policy normalization, including potential rate cuts, will exert downward pressure on interest rates across the yield curve. This declining rate environment will likely set the stage for a broadening of earnings growth beyond the dominant U.S. large-cap growth companies that have led the market in recent years.

Importantly, our portfolio strategy is adapting to these changing conditions. In our equity strategy, we are actively diversifying our portfolio beyond the most concentrated market positions. As interest rates normalize, we anticipate potential opportunities for earnings growth to broaden beyond the dominant U.S. large-cap growth sector. This approach aims to capitalize on emerging prospects across a broader range of market segments, potentially benefiting from the evolving economic landscape and shifting monetary policy environment. Within fixed income, we are becoming more receptive to taking on additional interest rate risk in our fixed income allocation, particularly as the 10-year U.S. Treasury yield has climbed back above 4.5%. This shift reflects our view that traditional fixed-income investments are poised to offer more effective diversification for our portfolios’ return-seeking assets in the coming year.

However, we remain vigilant and selective in our approach. While we see opportunities in fixed income, we are cautious about the recent compression of high-yield spreads, which have narrowed considerably. This development warrants careful consideration in our ongoing portfolio management and risk assessment. As we navigate this evolving landscape, our focus remains on balancing potential returns with prudent risk management, seeking to capitalize on emerging opportunities while maintaining a diversified and resilient portfolio structure.

As interest rates decrease, we expect a more balanced market performance, with potential gains extending to a wider range of sectors and asset classes. This shift could provide investors with expanded opportunities for both growth and income in their portfolios.

As we conclude our market outlook for 2025, we extend our heartfelt gratitude for your continued trust and partnership. Your confidence in our expertise has been the cornerstone of our shared success. While the economic landscape presents both challenges and opportunities, we remain committed to navigating these waters with diligence and insight on your behalf.

We wish you and your loved ones a prosperous, happy, and healthy New Year. May 2025 bring you financial growth, personal fulfillment, and joy in all your endeavors. As always, we look forward to working closely with you in the coming year to help you achieve your financial goals and secure your financial future. Thank you once again for your valued relationship. Here’s to a bright and prosperous 2025!

This material is for informational purposes only and is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Diversification cannot assure profit or guarantee against loss. There is no guarantee that any investment will achieve its objectives, generate positive returns, or avoid losses. Sequoia Financial Advisors, LLC makes no representations or warranties with respect to the accuracy, reliability, or utility of information obtained from third-parties. Certain assumptions may have been made by these sources in compiling such information, and changes to assumptions may have material impact on the information presented in these materials. Sequoia Financial Advisors, LLC does not provide tax or legal advice.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets