Stocks Make New Highs on Positive, but Slowing, Earnings

by Sequoia Financial Group

by Sequoia Financial Group

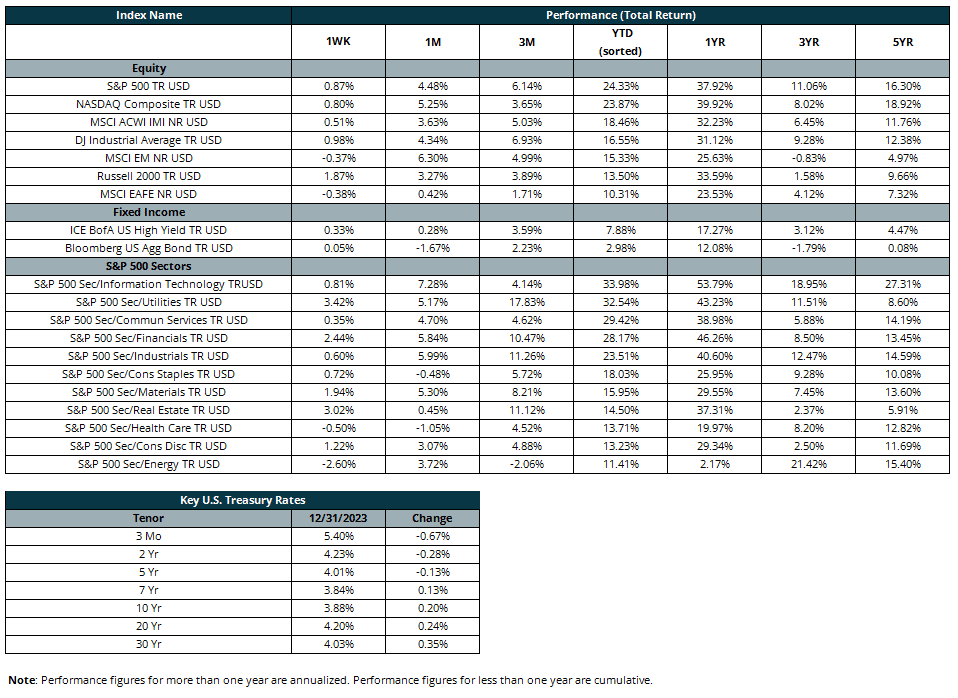

Both the S&P 500 Index and the Dow Jones Industrial Average surged to new record highs on Friday, sealing six straight weeks of gains. This marked the longest string of weekly advances in 2024 for the two indices. The three major averages clinched their sixth straight positive week.1

For the week, the Dow and S&P 500 rose 0.98% and 0.87%, while the NASDAQ climbed 0.80%. Small caps outperformed as the Russell 2000 Index rose 1.87%. Value stocks gained ground on growth stocks as the Russell 1000 Value Index rose 1.13%, besting the 0.73% gain in the Russell 1000 Growth Index. However, they lag on a year-to-date basis by a significant margin.2

Fixed-income markets rose marginally, with the Bloomberg US Aggregate Bond Index higher on the week by 0.05%.2 The US 10-year Treasury Bond remained unchanged on the week at 4.08%.3

Trading activity for the week was driven by third-quarter corporate earnings reports. Standouts this week came from a variety of industries, including: United Airlines (posting an earnings and revenue beat and announcing a stock buyback); Morgan Stanley (beating analysts’ forecasts on higher profits from its wealth management, trading and investment banking divisions), warehouse REIT Prologis (posting better-than-expected earnings, with the CEO commenting that the supply picture is improving, and the long-term demand drivers for the business remaining strong)4, and Netflix (following the video-streaming giant’s better-than-expected 3Q results and momentum in its ad-supported membership tier, which jumped 35% quarter over quarter)5.

At this early stage, earnings season is off to a mixed start. Overall, 14% of the companies in the S&P 500 have reported actual results for Q3 2024 to date. While the percentage of S&P 500 companies reporting positive earnings surprises is above the five- and 10-year averages at 79%, the size of the earnings surprises at 6.1% is below the five- and 10-year averages. For Q3 2024, the blended (year-over-year) earnings growth rate for the S&P 500 is forecast to be 3.4%. If this is the actual growth rate for the quarter, it will mark the fifth straight quarter of year-over-year earnings growth for the Index.6

Financial markets were also bolstered this week with favorable economic data. Consumer spending held up in September, underscoring a resilient economy that is now getting a boost from the Federal Reserve, the Commerce Department reported Thursday. Retail sales increased a seasonally adjusted 0.4% on the month, up from the unrevised 0.1% gain in August and better than the 0.3% Dow Jones forecast, according to the advance report. Meanwhile, on the labor front, initial unemployment claims filings totaled a seasonally adjusted 241,000, a decline of 19,000 and lower than the estimate for 260,000, the Labor Department reported.7

As equity markets continue to hit new highs, investors need to be mindful of valuations. With earnings growth seeming to slow in the third quarter, the forward 12-month P/E ratio for the S&P 500 is currently 21.9x, based upon 12-month forward earnings growth expectations of approximately 13%. This P/E ratio is above the five-year average of 19.5x and above the 10-year average of 18.1x.6

Sources:

- https://www.cnbc.com/2024/10/17/stock-market-today-live-updates.html

- Morningstar Direct

- https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_yield_curve&field_tdr_date_value=2024

- https://www.cnbc.com/2024/10/16/stocks-making-the-biggest-moves-midday-ual-ms-asml-pld-and-more.html

- https://www.cnbc.com/2024/10/18/netflix-shares-jump-5percent-in-premarket-after-third-quarter-earnings-beat.html?&qsearchterm=netflix

- https://insight.factset.com/sp-500-earnings-season-update-october-18-2024

- https://www.cnbc.com/2024/10/17/retail-sales-rose-0point4percent-in-september-better-than-expected-jobless-claims-dip.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets