Strong Earnings, Softer Tariff Talk Propel Stocks to New Highs

by Sequoia Financial Group

by Sequoia Financial Group

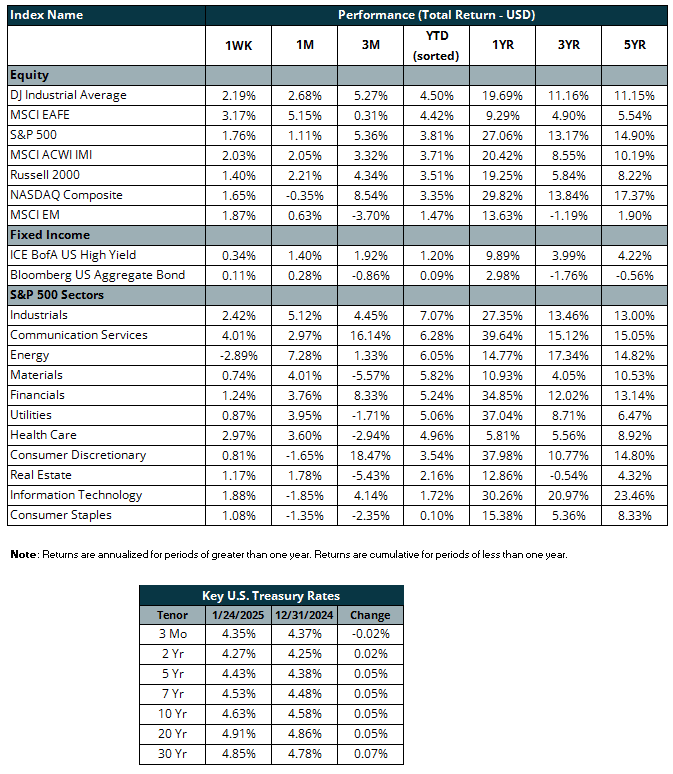

President Trump had pledged to slap 25% tariffs on goods imported from Mexico and Canada on Day One of his presidency, as well as tariffs of 60% or higher on goods coming from China. However, since taking office last Monday, Trump’s tariff announcements have been somewhat softer than expected. A decision on Mexico and Canada has been pushed off until February, and Trump stated in a recent interview that he’d rather not put tariffs on China. [1] [2] With new tariffs possibly adding to inflation and detracting from GDP growth, their delayed implementation was cheered by stock market investors. Indeed, the Dow Jones Industrial Average jumped more than 500 points on the first trading day of Trump’s second term.[3]

Strong fourth quarter earnings reports also provided a lift to the major market indices. Following upbeat banking reports two weeks ago, a more diversified mix of companies delivered positive results last week. For example, 3M – which has been hampered by litigation concerns in recent years – eased past analyst estimates and returned to positive organic growth.[4] Meanwhile, Charles Schwab grew revenue 20% year over year and announced it will expand its branch network by adding more than 12 new investor centers.[5]

Netflix added to the market’s momentum. Its shares jumped more than 9% after reporting that its paid-subscriber base has topped 300 million.[6] To put that number in perspective, the entire population of the United States didn’t top 300 million until 2020. Nvidia and Oracle also spiked on news that a joint venture between OpenAI, Oracle, and Softbank will invest $500 billion in AI infrastructure in the US. The tech-heavy NASDAQ rallied more than 1% on Wednesday, while the S&P 500 reached an all-time high.[7] For the week, the S&P 500 and NASDAQ each gained 1.7%.

Bonds haven’t enjoyed the same early-year success. A recent report by BkackRock argued that interest rates could stay higher for longer due to persistently large deficits and record Treasury issuance.[8] Meanwhile, Trump told the World Economic Forum he will demand lower interest rates globally. The Federal Reserve is not expected to cut its benchmark interest rate until at least May[9], setting up a possible showdown between Trump and Chairman Powell. For the year through January 24, the Bloomberg Aggregate Bond Index is little changed, as is the 10-year Treasury yield.

Looking ahead, earnings will remain in focus as Tesla, Starbucks, Meta, Microsoft, Apple and others report year-end results this week. We’ll also get a fresh look at inflation and GDP, in what will be a very busy news week for the financial markets.

[1]https://finance.yahoo.com/news/trump-avoids-big-tariff-actions-on-day-one-but-he-promises-they-could-be-days-away-202259180.html

[2] https://www.taipeitimes.com/News/front/archives/2025/01/25/2003830802

[3] https://www.cnbc.com/2025/01/20/stock-futures-rise-as-trumps-second-term-begins-live-updates.html

[4] https://investors.3m.com/news-events/press-releases/detail/1874/3m-reports-fourth-quarter-and-full-year-2024-results

[5] https://investors.3m.com/news-events/press-releases/detail/1874/3m-reports-fourth-quarter-and-full-year-2024-results

[6] https://www.cnbc.com/2025/01/21/netflix-nflx-earnings-q4-2024.html

[7] https://www.cnbc.com/2025/01/21/stock-market-today-live-updates.html

[8] https://www.blackrock.com/us/individual/insights/blackrock-investment-institute/weekly-commentary

[9] https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html?redirect=/trading/interest-rates/countdown-to-fomc.html

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

")

Fed Chair Powell’s Tariff Talk Spooks Already-Nervous Markets